“Milliseconds matter” is one of the most repeated claims in trading-infrastructure marketing, and it’s true — but only for some traders. A millisecond of latency is decisive if you’re scalping or running fast bots, and completely irrelevant if you hold positions for days.

So the useful question isn’t whether milliseconds matter in the abstract; it’s how much they cost your execution, and whether that’s enough to care about. Here’s the honest, quantified answer: how a delay actually degrades a fill, what it’s worth in real money, and how to tell whether latency is your problem or a distraction from one.

How a millisecond actually degrades a fill

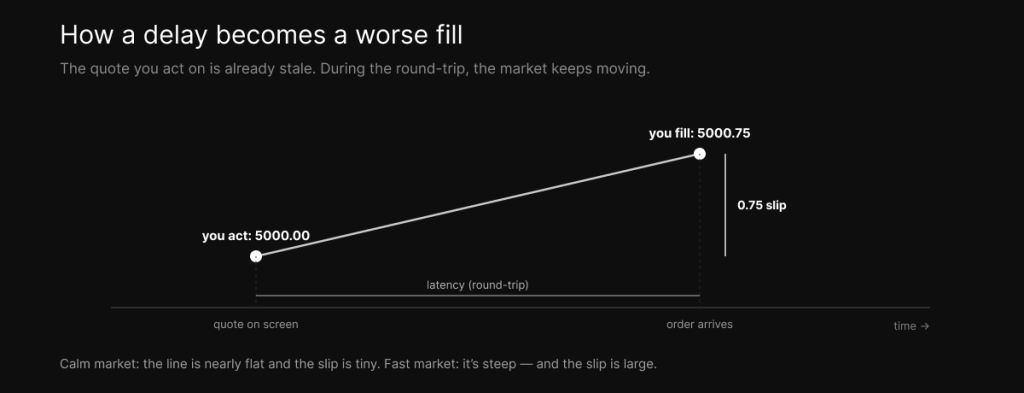

Latency hurts execution through a specific chain. The quote your platform shows you is already milliseconds old, and by the time your order travels to the exchange, the market has moved — so you fill at a price you never saw. That’s slippage, and latency is its most invisible cause, leaving no trace except a slightly worse fill, the mechanism we break down in can a VPS reduce slippage.

In fast markets the outcomes get worse. A limit order can have the price move past it before it arrives — a missed fill — or your limit becomes marketable and you pay the taker fee instead of earning the maker rebate. In a price-time-priority order book, even a tiny delay pushes your order back in the queue, lowering your odds of getting filled at your price. And a delayed stop activates late, turning a small loss into a bigger one. None of these shows up labeled “latency” on your statement; they just quietly make your trading worse.

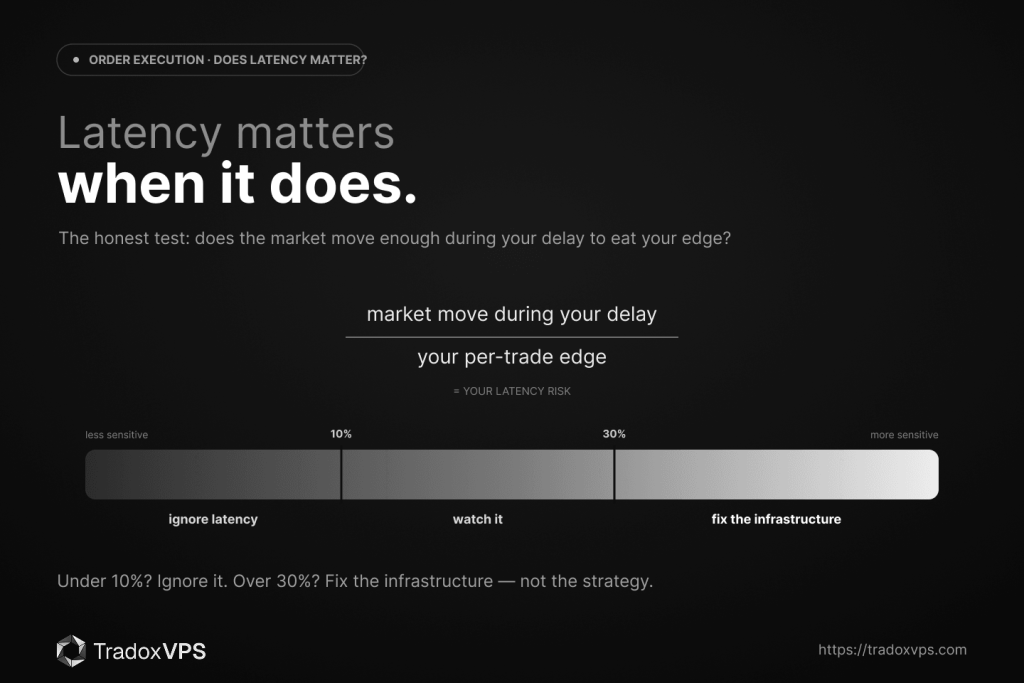

The honest part: latency matters relative to how fast the market moves

Here’s what most “milliseconds matter” pitches leave out: the damage depends entirely on how fast the market moves relative to your delay. On a slow-moving asset, 200 ms is negligible — the price hasn’t moved enough in that time to matter. On a volatile asset during an active session, 200 ms can be several price updates and a completely different market context than the one that generated your signal. So latency isn’t a fixed cost; it’s latency relative to your strategy’s signal window, the period during which your edge is valid.

There’s a clean way to decide whether it’s hurting you. Estimate how much the market moves during your execution delay, and divide it by your per-trade edge. If that ratio is under about 10%, latency isn’t your problem. If it’s over about 30%, it is — and no amount of strategy refinement will fix an edge that’s being eaten by execution delay. That single calculation matters more than any absolute millisecond number, and it’s the honest filter the low-latency tiers piece is really about.

What it costs in real money

When it does matter, the cost is real and it compounds. A controlled test of two identical automated strategies on the same pair found that the low-latency setup, under 1 ms, ran near break-even on slippage, while the high-latency one at 75 ms bled about 1.7 pips over 120 trades — roughly $170 at one lot, scaling toward five figures a year at size. The arithmetic is simple: slippage per trade times size times number of trades, so the faster you trade and the more size you carry, the more latency taxes you.

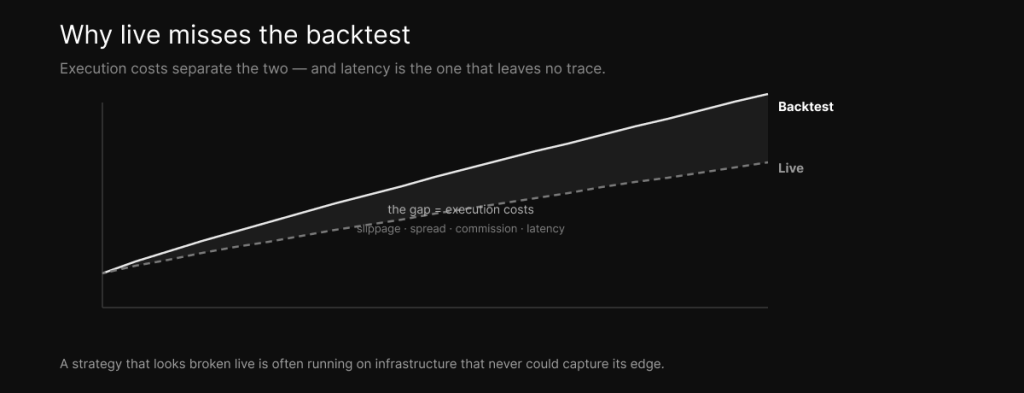

It also explains the single most common trading frustration — why live results miss the backtest. A backtest that ignores latency overestimates performance, because in the test your orders fill instantly at the signal price. Live, they don’t. A strategy that looks broken in real trading is very often running on infrastructure that was never capable of capturing its edge in the first place, which is the case the low-latency-execution piece makes from the solution side.

Does a millisecond matter for you?

It depends entirely on how you trade, and being honest about which row you’re in saves you either money or a broken strategy.

| Trader type | Does a millisecond matter? | Latency that’s “enough” |

|---|---|---|

| HFT / latency arbitrage | Decisive — races run in µs–ms | sub-1 ms (colocation) |

| Scalpers / fast bots | A lot — slippage compounds fast | 1–5 ms (proximity VPS) |

| News traders | Sharp, during releases | under ~20 ms |

| Active intraday / EA | Moderate — matters in fast markets | single-digit to ~20 ms |

| Swing / position | Essentially no | 100 ms+ is fine |

“Milliseconds matter” is true but conditional. If you’re a swing trader, optimizing for the last millisecond is wasted money — your edge lives on a timescale where it’s pure noise, and uptime matters far more. If you’re a scalper, that same millisecond is the difference between a strategy that works and one that doesn’t, which is exactly why the HFT and low-latency reality and matching your location to your strategy come down to how sensitive you actually are.

It’s consistency, not just speed

One thing the averages hide: jitter — inconsistent latency — is often more damaging than a slow average. A connection that delivers a steady 30 ms beats one that averages 10 ms but spikes to 200 ms during volatility, because those spikes land exactly when the market is moving fastest and a stale fill costs the most. So track your latency distribution, not just the mean — a wide gap between your best and worst readings is a warning sign, and it’s the real point of network speed versus latency: a predictable connection beats an occasionally fast one.

Measure the right number

Two measurement traps to avoid. First, ping is not your latency. A ping measures only the network leg to the server, while what actually affects your fill is the full round-trip from order sent to fill confirmed, which includes your broker’s processing. Use your broker’s execution report or a proper round-trip tool rather than ping alone, and keep in mind that the sub-millisecond figures in marketing — ours included — are ping, not execution.

Second, latency is only one of four execution costs, alongside slippage, spread, and commissions. A millisecond saved won’t rescue a strategy whose real problem is a wide spread, an oversized order, or an edge that was never there. Fix the cost that’s actually hurting you, not the one that’s easiest to market against.

The bottom line

Do milliseconds matter for order execution? Yes — if you trade fast enough that the market moves meaningfully during your delay. For scalpers, fast bots, and news traders, latency is a real, compounding cost that surfaces as slippage and missed fills, and cutting it is among the highest-ROI infrastructure decisions you can make. For swing and position traders, it’s noise, and chasing it is a distraction from uptime and strategy.

The honest move is to measure your real round-trip, estimate how much the market moves during it relative to your edge, and fix the infrastructure only if the number is uncomfortable. For latency-sensitive futures strategies, that usually means getting near the exchange — which is what the Chicago plans and pricing are built around. For everyone else, save the money and trade your edge.

Frequently asked questions

Yes — a delay means the quote you acted on is already stale, so the market can move before your order arrives, causing slippage, missed fills, or a delayed stop. How much it matters depends on how fast the market moves relative to your execution delay.

It’s slippage per trade times size times number of trades. A controlled test found a 75 ms setup lost about 1.7 pips over 120 trades versus a sub-1 ms setup — roughly $170 at one lot — and it compounds with frequency and size into thousands a year for active traders.

No. They’re decisive for HFT and scalpers, sharp for news traders during releases, and essentially irrelevant for swing and position traders, whose edge lives on a timescale where milliseconds are noise. Match your concern to your strategy.

Estimate how much the market moves during your execution delay, divided by your per-trade edge. Under about 10% and latency isn’t your problem; over about 30% and it is, and no strategy tweak will fix it. Checking your average slippage over 30 days helps too.

Often latency. A backtest that ignores execution delay overestimates performance, and a strategy that looks broken live may be running on infrastructure that was never fast enough to capture its edge. Latency is the most invisible execution cost.

Frequently, yes. Jitter — inconsistent latency — is often more damaging than a higher but steady average, because spikes hit during volatility when fills matter most. Track your latency distribution, not just the average.

No. Ping measures only the network leg to the server; your real latency is the full round-trip from order sent to fill confirmed, including the broker’s processing. Advertised sub-millisecond figures are ping, not execution.

We operate TradoxVPS and provide trading infrastructure, not financial advice. Latency reduces some execution costs but cannot eliminate slippage, spread, or a lack of edge; advertised sub-millisecond figures are network ping rather than order execution, and no infrastructure guarantees profitability. Trading futures and other leveraged products carries substantial risk, including the loss of more than your initial deposit.