Ask ten VPS providers what “low latency” means and you’ll get ten sub-millisecond numbers, every one of them designed to end the conversation before it starts. The honest answer is more useful: low latency isn’t a single number — it’s a spectrum, and what counts as “low” depends entirely on who you are and what you trade. A high-frequency firm and a retail day trader live in completely different latency worlds, separated by a factor of a thousand and roughly fifty thousand dollars a month.

So here’s the real picture: what latency actually measures, the three tiers it comes in with real numbers, what’s realistically “low” for the way you trade, and why the sub-millisecond figure on a sales page isn’t the one that fills your orders.

First, what “latency” actually measures

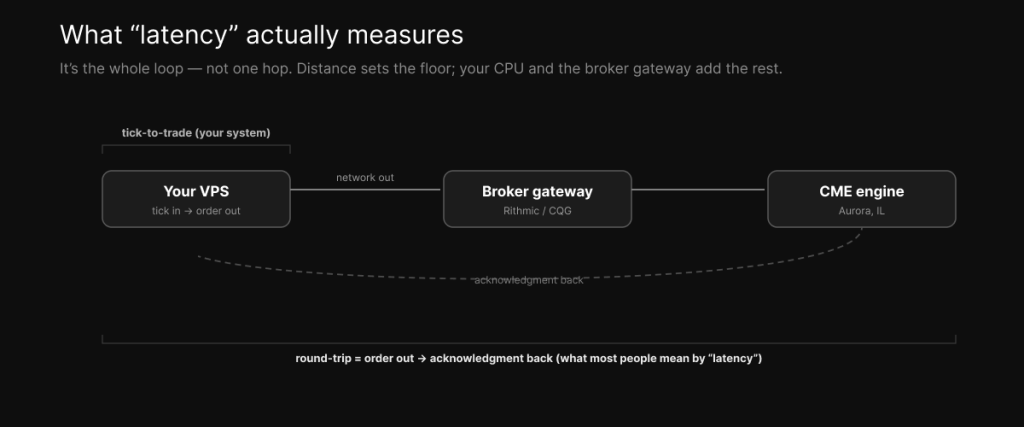

Latency is the time for a full loop, not a single hop. Your platform receives a market-data tick, your logic decides, the order travels to the exchange’s matching engine, and an acknowledgment comes back. Two terms are worth keeping straight. Tick-to-trade is the time from receiving a tick to sending an order — your own system’s internal speed. Round-trip is the full loop, from sending the order to getting the acknowledgment back. When people say “latency,” they almost always mean the round-trip, and it’s the sum of four things: the network distance, your processing, the broker’s gateway, and the exchange itself. Distance sets the floor; everything else stacks on top. (This is also why bandwidth and latency are not the same thing, which we untangle in network speed versus latency.)

The three tiers of “low latency”

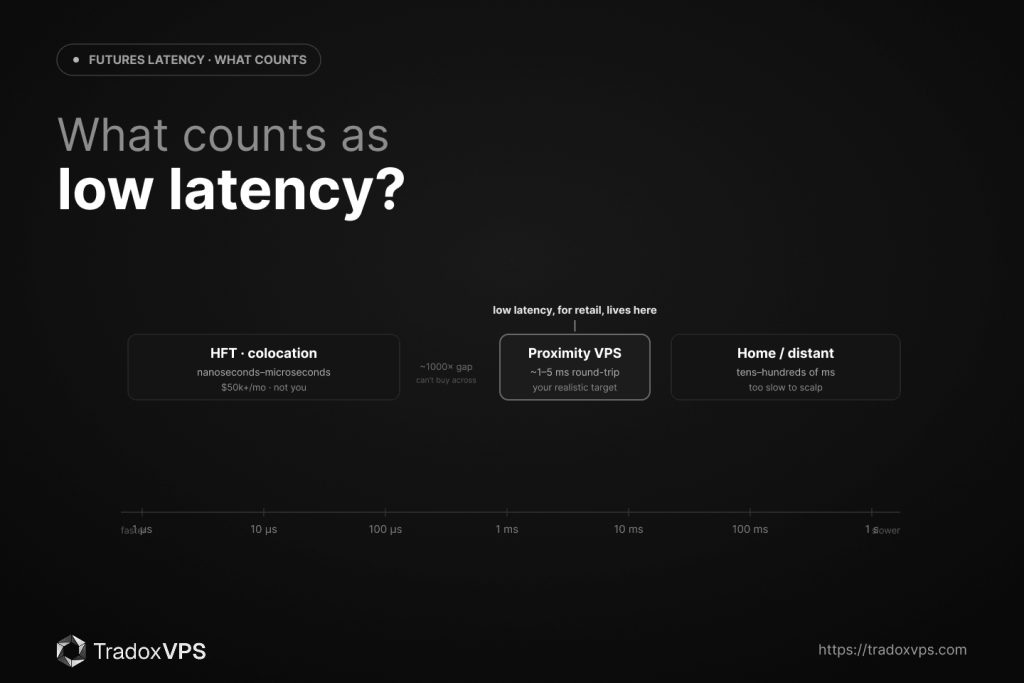

There isn’t one bar labeled “low.” There are three different worlds, and they’re worth seeing side by side.

| Tier | Typical latency | Who it’s for, and how it’s achieved |

|---|---|---|

| Ultra-low (HFT) | Nanoseconds to single-digit microseconds (tick-to-trade) | HFT and market-making firms; FPGA hardware, kernel-bypass software, colocation inside the exchange data center, microwave links. ~$50,000+/mo. |

| Proximity (active retail / prop) | ~1 ms network ping; ~3–5 ms order round-trip | Active retail and prop traders; a VPS near the exchange (Chicago for CME). ~$40–400/mo. |

| Standard retail | ~50–300+ ms | A home connection or distant cloud; retail (consolidated) data feeds rather than direct ones. Effectively free. |

The thing to absorb from that table is the size of the gaps. The jump from the top tier to the middle is roughly a factor of a thousand and tens of thousands of dollars a month, and here’s the part the marketing won’t tell you: a retail trader cannot buy into the top tier, and doesn’t need to. The realistic, sensible target for retail and prop traders is the middle row — single-digit-millisecond round-trip, kept consistent.

So what’s “low latency” for you?

It depends on your strategy, and matching the two is the entire point of this exercise.

HFT and market-making need microseconds, which means colocation and FPGAs — institutional territory. If you’re reading an article like this one, that isn’t you, and that’s completely fine.

Scalping benefits from single-digit milliseconds, under roughly 5 ms round-trip, and even more from low jitter, because you’re trading the fast moments where consistency of fills is what protects the edge. A proximity VPS is the right tool here.

Discretionary day trading is well served by under about 10 ms. Past that you’re optimizing something your own reaction time already dwarfs by orders of magnitude.

Swing and position trading barely care about latency for entries, since you’re holding for days, though it still affects stop-loss execution and gap risk, so it never quite drops to zero.

The realistic ceiling for retail is worth stating plainly: a proximity VPS gets you latency comparable to a small proprietary trading firm, which is more than enough for everything except true HFT.

The number on the sales page isn’t the number that fills your order

This is where most latency marketing quietly misleads, so three honest corrections.

Sub-millisecond is ping, not execution. A figure like “under 0.52 ms” or “0.82 ms to the CME” is the network leg to the data center — real, but it’s the ping, not your order’s round-trip through the broker, which lands in single-digit milliseconds. The headline measures the easy part of the loop, as we spell out in how a low-latency VPS improves execution.

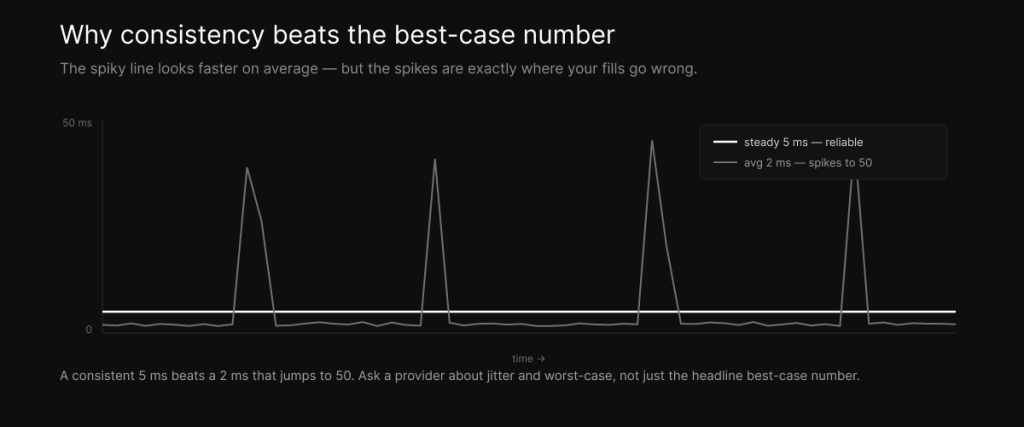

Jitter matters more than the average. A system that is consistently 5 ms beats one that averages 2 ms but spikes to 50 ms, because those spikes are exactly where your fills go wrong and where your live results stop matching your backtest. Ask a provider about consistency and worst-case, not just the best-case number.

Your data feed counts too. A retail, consolidated data feed can lag a direct exchange feed by 150 to 500 ms, so you can have a genuinely fast connection and still be trading on stale prices. Low latency is a property of the whole path, not just the order leg.

What actually makes latency low

The levers that move real latency, in order of how much they matter:

- Distance, the big one. Be near the matching engine — Chicago and Aurora for CME futures. The wrong city adds 15 to 25 ms, which is the whole argument in why a Chicago VPS is best for CME futures.

- A processor that keeps up. A slow CPU adds its own delay during volatility, when the tick rate spikes and a backlog forms — the tick queue.

- A clean, consistent route, which beats raw bandwidth every time.

- Direct feeds and a fast broker gateway, Rithmic or CQG, the last legs of the loop.

This is exactly what a proximity VPS is built to optimize — not to chase HFT microseconds, but to land you in the realistic low-latency tier without a $50,000 colocation bill, and it’s why those milliseconds turn into fewer ticks of slippage.

The honest bottom line

For a retail or prop futures trader, low latency means a single-digit-millisecond round-trip to your broker’s gateway, kept consistent, from a server near the exchange. It does not mean microseconds — that’s a different tier you can’t buy into and don’t need. So the right question isn’t “what’s the lowest number on the page?” but “is my latency low enough, and steady enough, for what I actually trade?” For nearly every non-HFT strategy, a proximity VPS answers yes, and you can see the Chicago plans and pricing if that’s the tier you’re after.

Frequently asked questions

For retail and prop traders, a single-digit-millisecond round-trip to your broker’s gateway, often around 3 to 5 ms, kept consistent, from a server near the exchange. True microsecond latency is institutional HFT territory, not a retail benchmark.

As a network ping to the exchange data center, yes, from a proximity VPS. But your actual order round-trip through the broker is single-digit milliseconds. The sub-millisecond figure is the network leg, not execution.

It depends on the strategy. HFT needs microseconds, scalping wants under about 5 ms, discretionary day trading is fine under about 10 ms, and swing trading barely notices. Home connections at 50 to 300 ms are too slow for genuinely latency-sensitive strategies.

Tick-to-trade is your own system’s internal time, from receiving market data to sending an order. Round-trip is the full loop, from sending the order to getting the acknowledgment back. Round-trip is what most people mean by “latency.”

No. A proximity VPS gets you into the active-retail and prop tier, single-digit milliseconds, which is plenty for non-HFT strategies. True HFT latency requires colocation and FPGAs costing tens of thousands of dollars a month.

Because random spikes cause unpredictable fills and break the match between your backtest and your live results. A consistent 5 ms is more reliable than a 2 ms that occasionally jumps to 50 ms.

No. Bandwidth and latency are different things. A fast home connection doesn’t place you near the exchange, and you may also be on a slower retail data feed, so your execution latency depends on the whole path, not your download speed.

We operate TradoxVPS and provide trading infrastructure, not financial advice. Latency figures are typical and vary with your broker, route, hardware, and configuration; a proximity VPS is not exchange colocation and does not deliver microsecond, HFT-grade latency. Trading futures and other leveraged products carries substantial risk, including the loss of more than your initial deposit.