In 2025, four researchers did something nobody selling a Polymarket course has done: they analyzed a full year of on-chain Polymarket order data and measured who was actually making money, and how. The study — Unravelling the Probabilistic Forest: Arbitrage in Prediction Markets — estimated roughly $40 million in realized arbitrage profit extracted during the measurement window. Not lucky calls on elections: systematic exploitation of pricing structure, by participants who treat Polymarket as a market rather than a sportsbook.

That’s the honest frame for “winning” here. The edge that persists isn’t predicting the news better than everyone — it’s understanding structure: how prices must relate to each other, where the platform pays you to participate, what fees and execution actually cost, and where your specific knowledge beats the crowd’s. This guide covers each, with the receipts, the math, and the risks the hype versions leave out.

What Polymarket is, mechanically

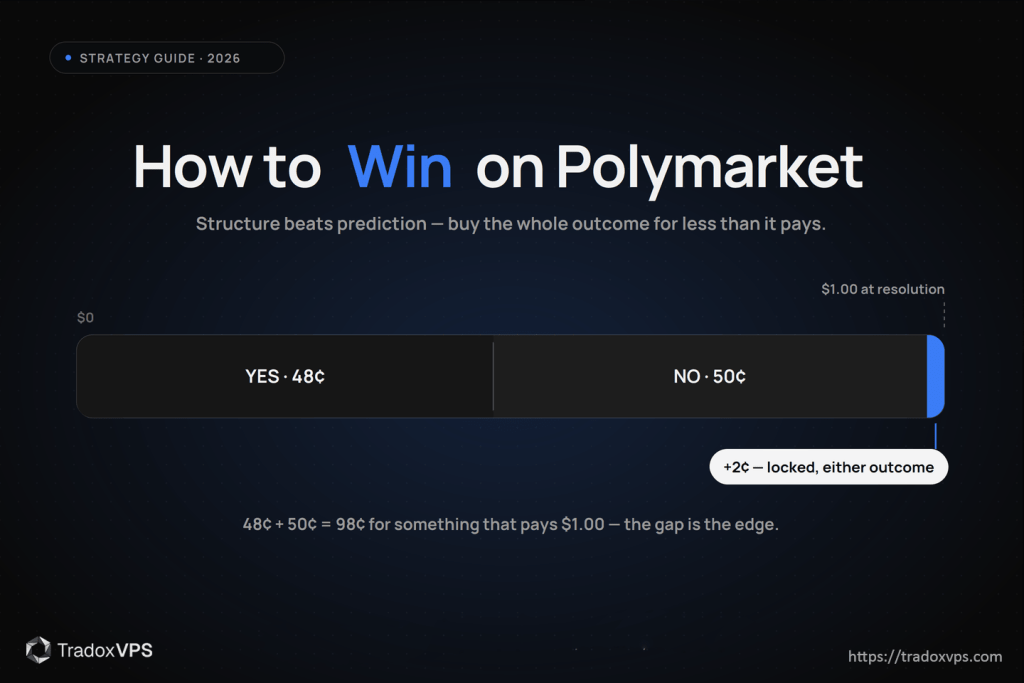

Polymarket is a peer-to-peer central limit order book on Polygon. Shares in an outcome trade between $0.00 and $1.00, the price doubling as the market’s implied probability; winners settle at $1.00, losers at zero. Resolution runs through UMA’s optimistic oracle rather than a central referee — which matters later, because oracle resolution has edge cases that strategy guides ignore. Since 2026 there are effectively two venues: the international book and a separate CFTC-licensed US exchange, with different fee schedules.

Prices here move on real capital, which is why they often front-run polls and headlines — and why the easy money you’ve heard about is mostly gone. What remains is below.

Strategy 1 — High-probability yield (“clear-win” markets), with the math done honestly

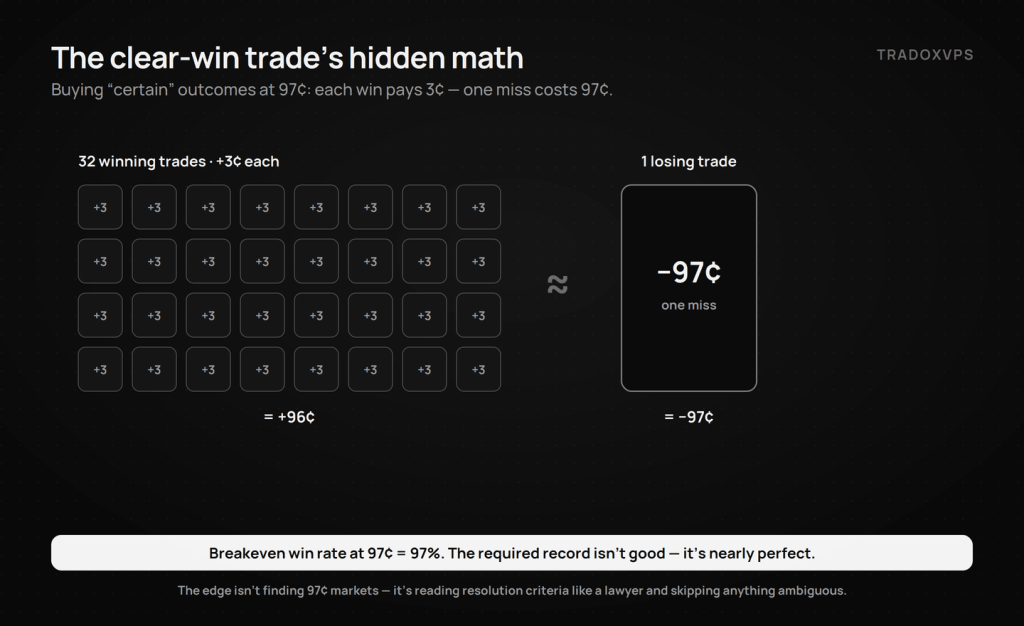

The setup: outcomes that are all but decided still trade at 95–98¢ while the world waits for formal resolution. Buying at 97¢ to collect $1.00 looks like a 3.1% yield, and on a market resolving in two weeks that’s substantial annualized. Two things the pitch always skips:

The blow-up math. At 97¢, you risk 97¢ to win 3¢ — one miss erases about 32 wins. “Virtually certain” markets fail in exactly the ways that don’t feel like market risk: a resolution-criteria technicality, a delayed event, an oracle dispute. So the real work isn’t finding 97¢ markets; it’s reading resolution criteria like a lawyer and skipping anything with interpretive wiggle. The win rate you need at these prices is not high — it’s nearly perfect.

The fee silver lining. Both major venues price taker fees on a curve that collapses toward zero at extreme prices (the formula is rate × P × (1−P) — full breakdown with worked examples in our arbitrage guide). Near 97¢, fees are pennies per hundred shares. The structure genuinely favors this strategy on costs; it punishes it on tail risk. Size accordingly.

Strategy 2 — Liquidity rewards, without the fantasy APY

Polymarket runs a liquidity rewards program that pays daily for posting competitive two-sided limit orders near the midpoint — you’re being paid to make the book deeper. It’s real, it’s the closest thing to “yield” on the platform, and it does not require predicting anything.

What it isn’t is free money, and we won’t quote you an APY — returns depend on the market, the reward pool, and how many other makers you’re splitting it with, all of which move. The honest cost of market-making is adverse selection: your resting orders get filled most eagerly precisely when the price is moving against them. News breaks, informed flow lifts your stale quote, and your reward income now sits beside an inventory loss. Serious LPs treat rewards as compensation for that risk, run tight quote-refresh logic (this is where automation stops being optional — a maker who updates quotes by hand is the stale quote), and track net P&L including inventory, not just the reward feed.

Strategy 3 — Mispricing where you actually know something

The crowd is good at headline probability and bad at fine print. Markets routinely misprice because participants haven’t read the resolution criteria, don’t understand a legal or procedural mechanism, or import emotion into a price. If you have genuine domain depth — election law, sports injury dynamics, how a specific agency announces data — your edge is largest in exactly the markets where that knowledge changes the resolution math. The discipline: trade your niche, write down your probability before looking at the market price, and pass when the gap is small. This is the one strategy on this page where a laptop and patience beat any bot.

Strategy 4 — Systematic participation, done inside the rules

Older versions of this guide — and plenty of others online — recommend scaling “volume farming” across dozens of accounts for incentives. We’re striking that advice: multi-accounting violates Polymarket’s terms of service, sybil patterns are exactly what incentive programs filter for, and the downside is forfeited funds and banned wallets, not a missed airdrop. If platform incentives reward genuine activity, earn them with one account doing real trading — rewards-program market-making and systematic strategies generate plenty of legitimate volume. An edge that depends on breaking the platform’s rules isn’t an edge; it’s a countdown.

The math layer: what the $40M study actually found

The arXiv paper is worth reading in full (it’s free); here is the trader-relevant core.

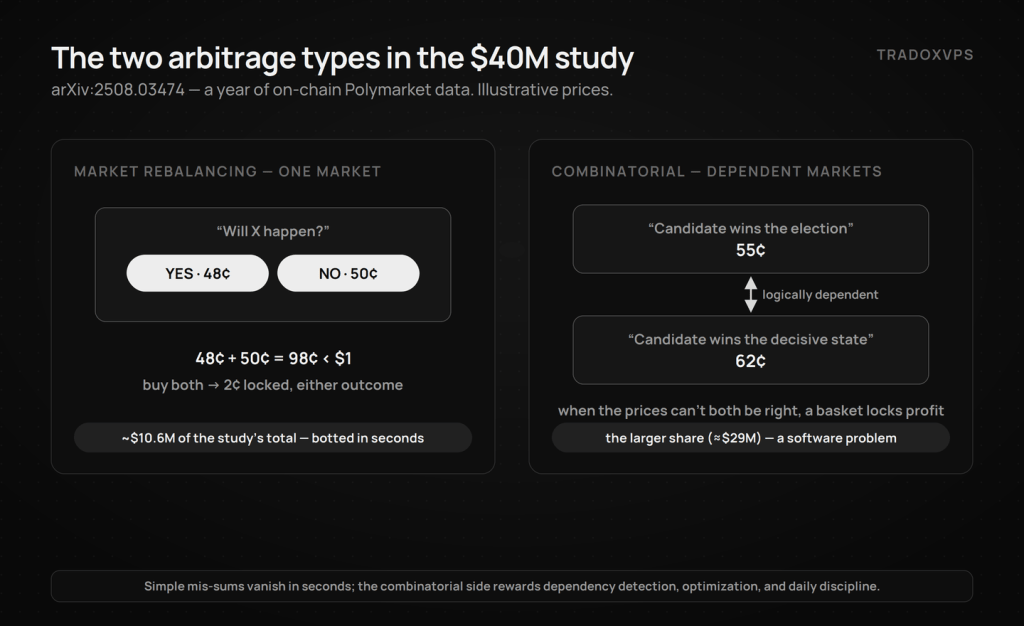

Two structures, not one. The researchers split extracted profit into Market Rebalancing Arbitrage — prices within a single market failing to sum to $1, the classic YES+NO < $1 trade — and Combinatorial Arbitrage across logically dependent markets. The simple intra-market kind accounted for roughly $10.6M; the larger share came from the combinatorial side, where, say, state-level election markets and the national market imply contradictory probabilities. If “candidate wins Pennsylvania” and “candidate wins the election” are priced inconsistently with how those events depend on each other, a basket exists that profits whichever way reality resolves.

The edge was small and systematic, not heroic. The most successful wallet in the study extracted about $2.0M across ~4,049 trades — roughly $500 per trade, compounded by showing up every day with tooling. The tooling matters because finding combinatorial inconsistencies across thousands of markets is a search problem: the researchers used embeddings and LLMs to detect dependencies between markets, then optimization methods (Frank–Wolfe with integer-programming oracles, Bregman projections) to compute the profit-locking basket. That stack is replicable by a serious individual in 2026 — the paper is effectively a blueprint — but it is software work, not clicking.

The execution-risk floor is in the paper too. The authors only counted opportunities with margins above $0.05, because thinner gaps get consumed by execution reality — fills, fees, movement between legs. That’s the academically grounded version of everything our cross-platform arbitrage guide says about fee curves, depth, and one-legged risk: the gross gap is the start of the math, not the end.

Execution: where speed actually matters, in measured numbers

Here’s where infrastructure vendors — historically including an older version of this page, which printed a fantasy table claiming “<1ms” — usually start lying. We benchmark our own boxes publicly instead, so the honest version costs us nothing:

- A human in a browser perceives the market through polling, rendering, and reaction time — the loop is measured in seconds, which is fine for Strategy 3 and hopeless for racing arbitrage.

- An automated bot on a WebSocket feed from a well-placed box sees book updates and round-trips orders in tens of milliseconds: in our June 2026 four-provider Dublin benchmark (raw data downloadable), live-feed medians ran ~13–15 ms and warm order-path medians ~21–23 ms — nobody measured 1 ms, including us.

- Between competing bots, races are decided in the tail, not the median: order-path p99 across the four boxes we tested ranged from 37 ms to 55 ms. When several systems chase the same resting contracts, the one whose worst moments are smallest wins the ties — which is why we publish p99s and worst samples, and why you should demand them from any provider.

The decision rule is the one from the arbitrage guide: wide, slow, persistent edges (clear-win yield, niche mispricing) need a browser and judgment; narrow, fast, contested edges (rebalancing arb, reward-program quoting, anything the study’s wallets were doing) need always-on automation with a short, measured path. Measure it yourself — the 20-minute probe runs on any box, including a free 3-day demo of ours.

Infrastructure, briefly — because this is a strategy guide

If your strategy needs automation, the requirements are mundane and specific: an always-on box (a sleeping laptop is a stale quote with your money behind it), one fast core for the parse-decide-sign loop, enough RAM that a news spike doesn’t OOM-kill your bot mid-position, and reconnect-and-resync logic on the V2 CLOB. A single-strategy bot runs comfortably on our $44.90 Starter (2 cores, 6 GB); the full sizing logic — what each resource does and what breaks first — is the VPS specs guide, the deployment walkthrough is the bot setup guide, and current tiers are on the pricing page. Windows Server or Ubuntu, your choice.

The risk paragraph every “win” guide should have

Execution risk: legs fill apart, prices move between them. Resolution risk: UMA disputes and criteria technicalities turn “certain” into contested. Lock-up: arb and yield profits realize at resolution, so judge everything annualized, against the next opportunity your capital can’t take. Fees: curve-shaped and category-dependent — model them per trade, not as a vibe. Platform risk: rules, fees, and reward programs change; strategies built on last quarter’s parameters decay. And concentration: at 97¢, one bad resolution erases a month. Nothing on this page guarantees profit; the study’s wallets won by sizing for all of the above, every day.

Frequently Asked Questions

Yes, in specific lanes: niche markets where you have genuine domain depth, careful high-probability yield with strict resolution-criteria reading, and rewards-program market-making run with real quote automation. The lanes that look easiest — racing arbitrage gaps manually — are the ones already industrialized by bots.

Researchers analyzing a year of on-chain data (arXiv:2508.03474) estimated ~$40M in realized arbitrage profit, split between simple intra-market mispricing (~$10.6M) and a larger combinatorial share across logically dependent markets. The top wallet averaged roughly $500 of profit per trade across thousands of trades — small, systematic, software-driven edges.

Not for judgment-based strategies — domain-expertise trading works from a browser. You do for anything time-competitive: arbitrage, liquidity-reward quoting, news-reaction strategies. A manual maker is, by definition, the stale quote informed flow feeds on.

They’re real daily payments for competitive two-sided quotes (official program details), and they’re best understood as compensation for adverse-selection risk — your quotes fill fastest when the price moves against you. Worth it for automated makers who track net P&L including inventory; not a passive yield product.

For automated, time-competitive strategies, yes — and the right way to evaluate it is measured numbers, not advertised ones. Our published Dublin benchmark shows ~13–23 ms medians with tails of 37–55 ms across four providers; anyone quoting sub-millisecond latency to Polymarket is marketing at you. Run the public probe on any box before paying.

No — multi-accounting violates Polymarket’s terms of service, and incentive programs actively filter sybil patterns. The realistic outcome is forfeited funds, not multiplied rewards. Everything in this guide works with one account.

Study figures from arXiv:2508.03474 (measurement window April 2024–April 2025); fee and program details link to official Polymarket pages and change over time — verify before trading. Latency figures from our June 2026 public Dublin benchmark. We operate TradoxVPS and provide infrastructure, not financial advice. Prediction market trading involves substantial risk, including total loss of capital.