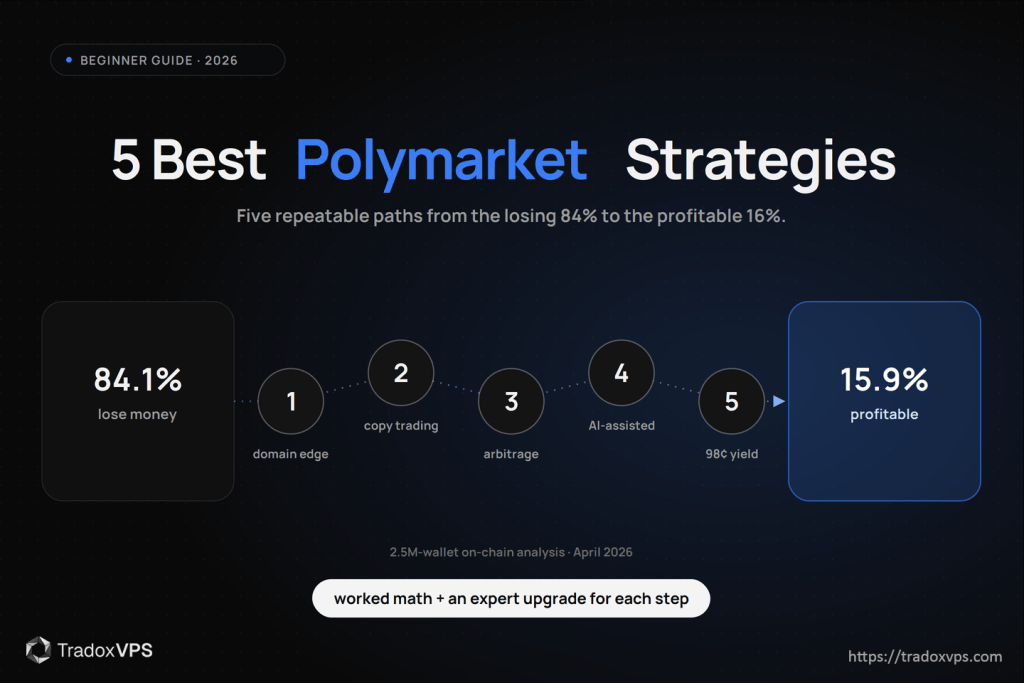

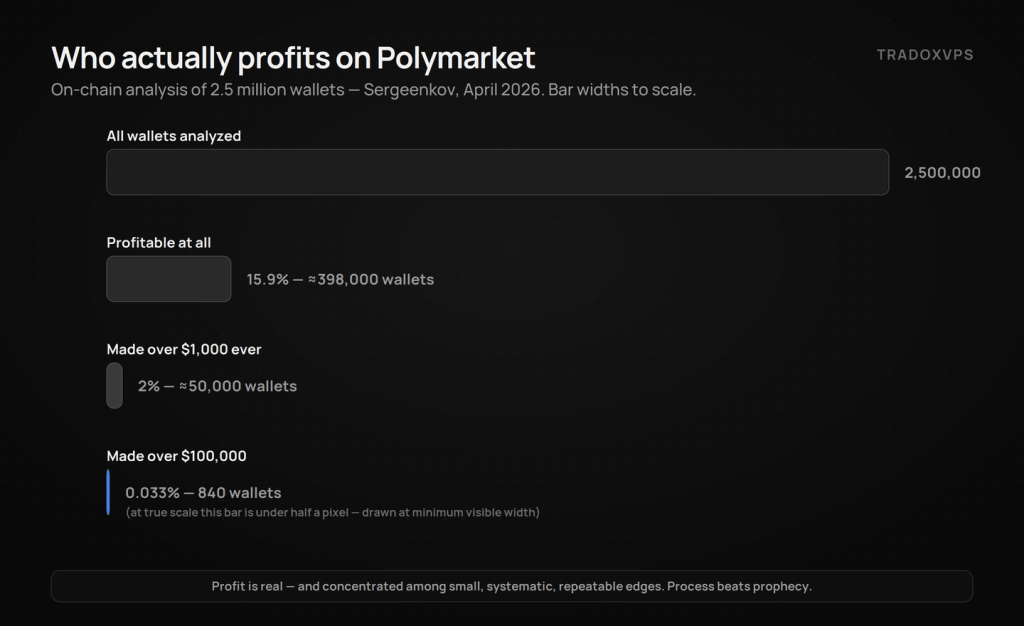

Here is the honest starting point that most strategy guides skip. In April 2026, on-chain researcher Andrey Sergeenkov analyzed 2.5 million Polymarket wallets by tracking every USDC flow through the platform’s settlement contracts: 84.1% of traders have lost money. Only 2% have ever made more than $1,000, and just 840 addresses — 0.033% — have cleared $100,000. An earlier 1.7-million-address study found the top 0.04% of wallets captured roughly 70% of all realized profits, and a Solidus Labs report found under 1% of wallets taking about half the gains in major political markets.

Those numbers aren’t a reason to leave. They’re a map. The same research notes that the winning minority skews heavily toward systematic approaches, while losing manual traders tend to enter after prices have already moved. So the question this guide answers isn’t “how do I pick winners?” — it’s “which repeatable systems put a beginner on the right side of an 84/16 split?” Five of them, each with the worked math, a beginner playbook, and the expert upgrade for when you outgrow it.

First, the mindset shift: you’re trading prices, not predicting events

Polymarket is a peer-to-peer exchange: orders match on a central limit order book and settle on-chain through the platform’s conditional-token contracts, with each share priced $0.00–$1.00 as the market’s implied probability. Nobody pays you for being right about the world; you get paid when your probability is better than the price. A market at 50¢ that should be 70¢ is a 20¢ edge; a market at 70¢ that should be 70¢ is a coin you’re flipping against fees. Every strategy below is a different repeatable way of finding that gap — and every beginner loss-pattern in the data is some version of buying the price after it already moved to fair.

The five strategies at a glance

| Strategy | Risk | Time/week | Sensible starting capital | Edge source | Automation needed? |

|---|---|---|---|---|---|

| 1. Domain-expertise trading | Medium | 5–10 hrs | $50+ | You know a niche better than the crowd | No |

| 2. Copy / mirror trading | Low-Med | 2–4 hrs | $100+ | On-chain transparency | Optional |

| 3. Cross-platform arbitrage | Low (per trade) | Varies | $500+ split across venues | Structural mispricing | Yes, at narrow spreads |

| 4. News & AI-assisted trading | Medium | 3–8 hrs | $100+ | Information processing | Only for racing |

| 5. Near-certain yield (“obvious NO”) | Low rate, high severity | 1–3 hrs | $500+ | Time-value + criteria reading | No |

Capital figures are practical guidance for making fees and lock-up worthwhile — not magic thresholds.

Strategy 1 — Domain-expertise trading: the only edge nobody can front-run

How it works. Pick the narrow slice of the world you understand better than a generalist crowd — a sport you’ve followed for a decade, a regulatory process you work inside, a country’s politics you read in the original language — and trade only there. Write your own probability down before looking at the market. If you’d put an outcome at 80% and the market prints 62¢, you’ve found an 18¢ gap; if the market prints 78¢, close the tab — no trade is a position too.

Beginner playbook. One niche, not five. Size every position at a small fixed fraction of your bankroll (the classic risk-management heuristic is 1–5% per idea — boring is the point). Keep a journal with three columns: your pre-price probability, the market price, the outcome. For the first 25–50 trades, your goal isn’t profit — it’s calibration: when you said 70%, did those events happen about 70% of the time? A calibrated trader with small size becomes a profitable trader with size; an uncalibrated one just donates faster.

Expert upgrade. Read resolution criteria like opposing counsel — most “shock” losses in expertise trading are criteria technicalities, not bad analysis. Anchor on base rates before narrative (how often do incumbents actually lose this kind of race?). And adopt an exit discipline: a position bought at 62¢ that reaches 85¢ has already paid you most of its edge — many experienced traders harvest there rather than sweat the last 15¢ through resolution risk. The data’s warning is blunt: manual traders lose mostly by arriving late — if the price already moved on your news, your edge went with it.

What kills it: trading outside your niche, confusing conviction with calibration, and overtrading because research feels like it deserves a position.

Strategy 2 — Copy and mirror trading: transparency is the product

How it works. Every Polymarket trade settles on a public blockchain, which makes the entire platform a glass building: any wallet’s full history — entries, exits, P&L — is inspectable. Beginners can systematically follow proven wallets instead of guessing. Start at the official leaderboard, filterable by timeframe and category; a whole ecosystem of third-party wallet trackers and copy-execution bots has grown around the same on-chain data.

Beginner playbook. Build a shortlist, then interrogate it: consistency across multiple recent windows (7-day and 30-day form, not lifetime totals — all-time leaderboards are full of one lucky market), enough trade count to mean something (dozens, not three), a recognizable category specialization, and survivable drawdowns. Mirror with small size and predefined exits — you can see their entries in real time, but you are not guaranteed to see their exits in time, so your risk rules must be your own.

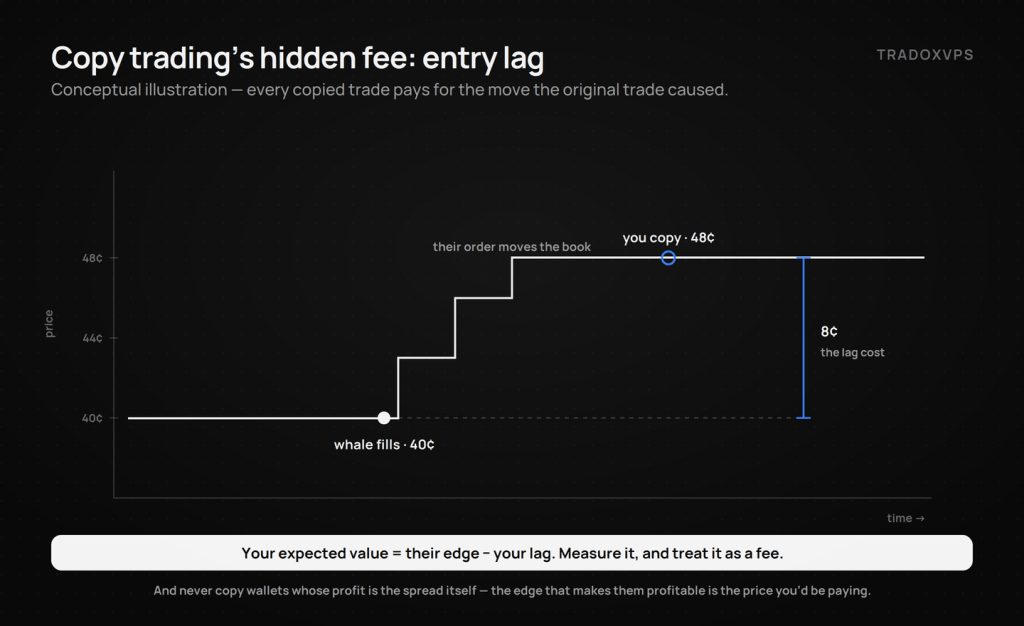

Expert upgrade — the three traps the on-chain data reveals. First, entry lag is your real cost: if a tracked wallet filled at 40¢ and the price prints 48¢ by the time you act, your expected value is theirs minus eight cents — measure your average lag and treat it as a fee. Second, don’t copy market-making bots: wallets grinding 15-minute crypto markets look spectacular on leaderboards, but their profit is the spread — the exact thing you’d be paying to follow them. Third, screen for insider-pattern wallets: an address with one or two enormous wins on hyper-specific events isn’t a system you can ride, it’s information you don’t have. And one security rule with no exceptions: any copy tool gets a dedicated wallet with capped allowances and never withdrawal permissions.

What kills it: chasing moved prices, decoy/wash wallets (analytics firms have flagged wash-trading patterns on the platform), and outsourcing judgment so completely you can’t tell when your source has gone cold.

Strategy 3 — Cross-platform arbitrage: the structural trade

How it works. Polymarket, Kalshi, and the smaller venues run independent order books, so the same event trades at different prices across them. The clean version: an event shows 60¢ YES on Polymarket while Kalshi prices the same outcome at 70¢ — you buy YES on Polymarket at 60¢ and NO on Kalshi at ~30¢ ($1 minus the YES price). Pair cost 90¢, payout $1.00 whichever way the event resolves: 10¢ locked, before fees.

Beginner playbook. Start manual, on wide gaps (5¢+) in slower markets, with three checks before any order: real book depth behind the headline price, the fee math on both legs, and matching resolution criteria on both venues. The full mechanics — scanner workflow, the 2026 fee formulas that peak exactly at 50¢, the one-legged-risk rule — live in our dedicated prediction market arbitrage guide; read it before your first pair.

Expert upgrade. Narrow gaps in liquid markets are an automated race; the academic analysis of a year of Polymarket data (arXiv:2508.03474 — the “$40M study” we break down in How to Win on Polymarket) only counted opportunities above a 5¢ margin precisely because execution reality eats the rest. Experts post maker legs to dodge taker fees, prefer fee-light categories, and size to top-of-book.

What kills it: one leg filling while the other moves, fees at mid prices, resolution divergence between venues, and capital sitting split across two platforms.

Strategy 4 — News and AI-assisted trading: analyst first, race car later

How it works. Prices adjust to news in stages — fast in headline markets, slowly in niche ones. Modern LLM tooling lets one person process more information than a 2020 trading desk: summarizing resolution criteria, pulling base rates, monitoring announcement schedules, and flagging markets whose prices haven’t digested a development yet.

Beginner playbook — AI as analyst, not trigger. Use models to structure your probability before you look at the price: “What’s the base rate for X? What exactly does this market’s resolution source say? What would have to be true for NO?” Then verify every factual claim against the primary source — a hallucinated detail is an unforced 100%-loss position. Your edge here is slower, deeper digestion of niche markets, not speed.

Expert upgrade. Automated news-reaction pipelines that reprice markets ahead of the crowd are real — and contested by professionals whose infrastructure is measured, not advertised. If you graduate to racing repricings, the requirements are mechanical: an always-on bot, WebSocket book mirrors, and a short measured path — our public Dublin benchmark shows what real numbers look like (~13–15 ms feed medians; races decided in the tails), and the same probe runs on any box you’re considering, including ours.

What kills it: trusting model output without source verification, and racing professionals on consumer Wi-Fi.

Strategy 5 — Near-certain yield (“obvious NO”): low risk per trade, ruinous when wrong

How it works. Markets on wildly unlikely outcomes often leave NO trading at 97–98¢ while the world waits for formal resolution. Buy at 98¢, collect $1.00: a ~2% absolute return, often over weeks — and one of the few strategies where the platform’s fee structure works for you, since taker fees collapse toward zero at extreme prices (the fee-curve math is in the arbitrage guide).

The math, honestly. At 98¢ you risk 98¢ to win 2¢: breakeven win rate is 98%, and a single miss erases ~49 wins. Judge every position annualized — 2% locked for 30 days is ~27% annualized and possibly excellent; 2% locked for a year is dead capital — and accept that the real job is eliminating ambiguity: this strategy only buys markets whose resolution criteria are mechanical, sourced, and already effectively determined. “Surely not” is not a criterion.

Beginner playbook: small, diversified across uncorrelated events, short windows first, criteria read in full. Expert upgrade: treat it as a portfolio with a velocity target (turnover × net spread), ladder resolutions so capital recycles weekly, and keep a hard cap on exposure to any single resolution mechanism — correlated “impossible” events have a way of failing together.

What kills it: one ambiguous market, one oracle dispute, one black swan — at 49:1 payoff asymmetry, the tail is the strategy.

Which strategy should you actually start with?

Have a genuine niche and 5+ hours a week → Strategy 1, with the calibration journal. Short on time but willing to do diligence → Strategy 2, small, with your own exit rules. Comfortable with spreadsheets and patient capital → Strategy 5 on short-dated, unambiguous markets. Strategies 3 and 4’s automated forms are graduation targets, not entry points — earn your way there with the manual versions first. Whichever you pick: one strategy, 25–50 journaled trades, tiny size, then judge yourself on calibration rather than P&L.

The five beginner mistakes the data keeps recording

- Casino sizing — the loss pattern behind most of the 84% is concentration, not bad picks. Fixed small fractions, always.

- Arriving late — buying the price after it moved is the documented signature of losing manual wallets. If you missed the move, you missed the trade.

- Copying entries without owning exits — mirrors see fills, not risk management.

- Trading ambiguous criteria — at any price, a market you can’t define is a coin flip wearing a costume.

- Confusing activity with edge — more trades isn’t more edge; the top wallet in the academic arbitrage study averaged ~$500 a trade across thousands of systematic trades, not heroic ones.

A short, honest word on infrastructure

Strategies 1, 2 (manual), and 5 need a browser and discipline — nothing else, and anyone telling a beginner otherwise is selling. The automated forms of 2, 3, and 4 need what any 24/7 system needs: an always-on box sized for the job (our $44.90 Starter — 2 cores, 6 GB — runs a single bot comfortably; the full sizing logic is in the VPS specs guide), deployment per the bot setup guide, and latency you’ve measured rather than believed — the benchmark and its 20-minute script exist for exactly that, and they work on a free 3-day demo before you spend anything.

Frequently Asked Questions

Per an April 2026 on-chain analysis of 2.5 million wallets, about 15.9% are profitable and 84.1% have lost money; only 2% have ever made more than $1,000, and 0.033% have cleared $100,000. Earlier studies found the top ~0.04% of wallets capturing around 70% of all realized profits. Profit on Polymarket is real — and extremely concentrated among systematic traders.

Domain-expertise trading in one niche you genuinely know, journaled and tiny, judged on calibration for the first 25–50 trades — or careful copy trading with your own exit rules if research time is the constraint. Both work from a browser with $50–100.

$50–100 is enough for Strategies 1 and 2. Arbitrage realistically wants $500+ split across two venues so fees and lock-up don’t dominate, and near-certain yield needs enough size for 2% spreads to matter. Capital never substitutes for calibration — fund the account after the journal says you’re ready.

The data is public and the approach is legitimate, but the risks are specific: entry lag erodes the copied edge, leaderboards are polluted by lucky one-market wallets and uncopyable market-making bots, and wash/decoy patterns exist. Vet for multi-window consistency, mirror small with your own exits, and never grant any tool withdrawal permissions.

No — three of the five strategies here are fully manual. Automation becomes necessary only when your edge depends on reaction time or 24/7 presence: narrow arbitrage, copy bots, news racing. Graduate to it; don’t start there.

The on-chain pattern is consistent: oversized positions, entries after the price already moved, ambiguous markets, and no measurement of their own calibration — while the profitable minority runs small, systematic, repeatable edges. The gap is process, not prophecy.

Profitability statistics from independent on-chain analyses (Sergeenkov, April 2026; DeFi Oasis, December 2025; Solidus Labs, April 2026) — linked above; methodologies differ and figures evolve. Fee and platform mechanics link to official sources and change over time. We operate TradoxVPS and provide infrastructure, not financial advice. Prediction market trading involves substantial risk, including total loss of capital.