Prediction markets are designed to aggregate beliefs about future events. What they’re not designed to do is stay in sync with each other. Polymarket, Kalshi, Limitless, Myriad, and Opinion each run independent order books, with their own liquidity, their own mix of market makers and retail flow, and their own lag in absorbing news. The result: the same outcome can trade at meaningfully different prices on two venues in the same second — and that gap is tradable.

This guide covers the mechanics, the two trade structures, where gaps come from, what eats your spread (with the actual 2026 fee formulas, not last year’s), the honest version of why latency matters, the risks nobody puts in the scanner, and the infrastructure question — including what our own measurements say about it.

How prediction market arbitrage works

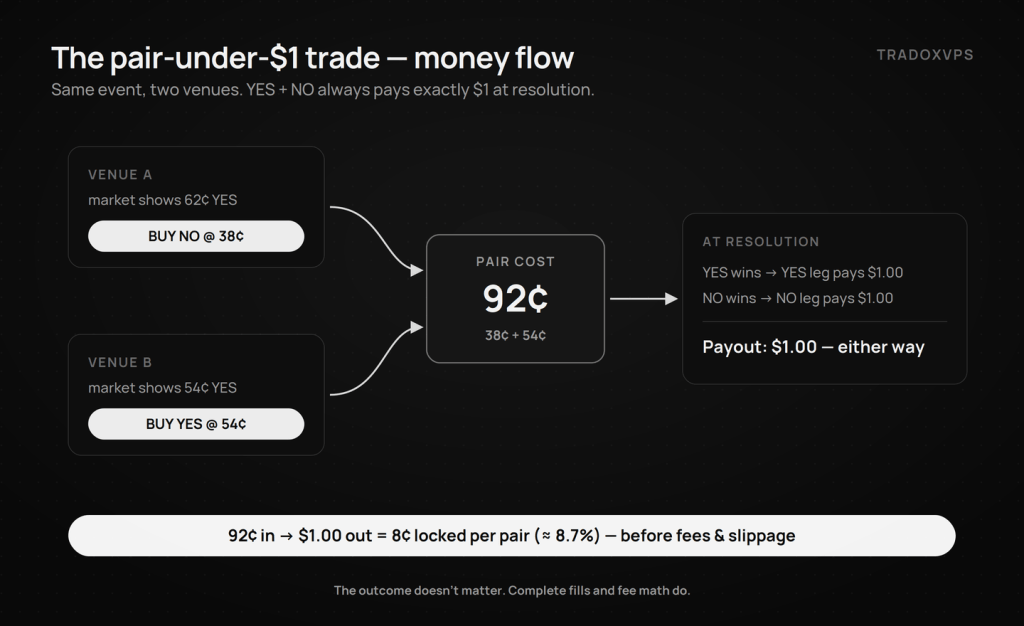

Every binary market resolves at exactly two values: $1.00 for the outcome that happens, $0.00 for the one that doesn’t. So a YES share and a NO share on the same event always sum to $1.00 at resolution — on every platform, every time. The arbitrage follows directly: if you can buy YES on one venue and NO on another for a combined cost under $1, the difference is locked in regardless of the outcome.

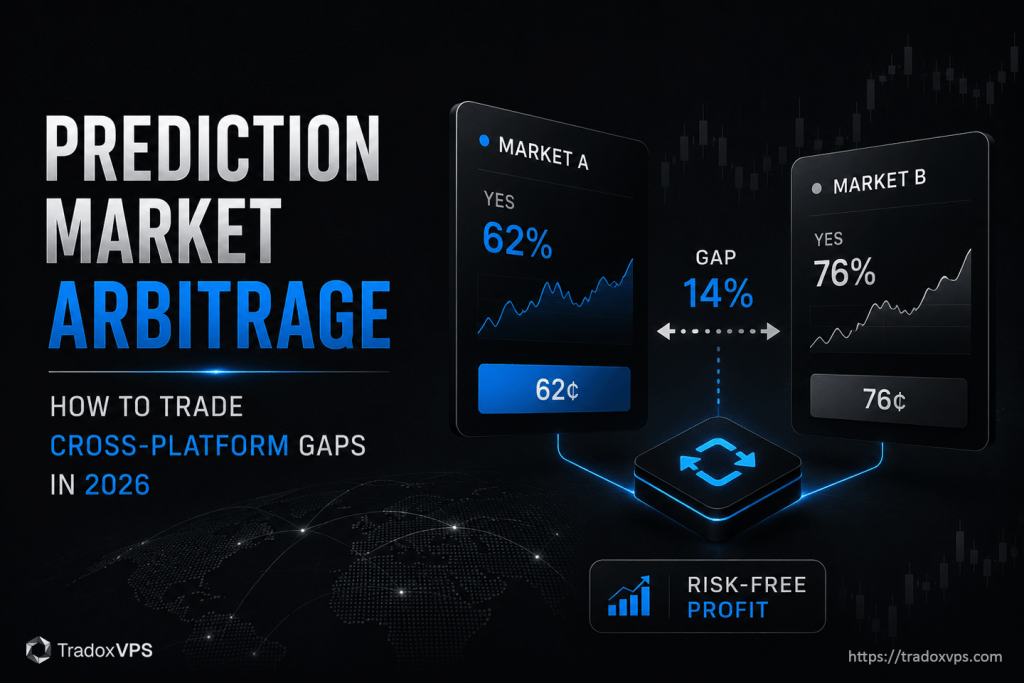

Clean worked example: an event trades at 62¢ YES on Platform A and 54¢ YES on Platform B. You buy YES on B at 54¢ and NO on A at 38¢ (NO costs $1 minus the YES price). Pair cost: 92¢. At resolution, exactly one of your two positions pays $1. Locked profit: 8¢ per pair — about 8.7% on committed capital, before fees, whoever wins.

A live illustration of how wide these can get: on May 26, 2026, the 0xinsider scanner showed a Ballon d’Or market with YES at 18.9¢ on Polymarket and NO at 44.9¢ on Myriad — a 63.8¢ pair paying $1, a 36.2¢ locked spread. Gaps that size carry their own warnings (thin books, long lock-up — both covered below), but they exist, and a scanner finds them in seconds.

The two trade structures

Type 1 — the pair-under-$1 trade. Buy YES on venue A at P₁, NO on venue B at P₂, with P₁ + P₂ < $1. Profit is $1 − (P₁ + P₂) in both states of the world. You need no opinion about the event — only complete fills and accurate fee math.

Type 2 — the same-side spread. When the same side trades at different prices — YES at 7.0¢ on one book and 7.5¢ on another — buy cheap and sell rich simultaneously; the positions cancel at resolution and the 0.5¢ is yours. The catch: selling requires shares or margin on the rich venue, and the two legs must fill together. If one leg fills and the other book moves, you’re holding a directional position you never wanted — the central execution risk of all arbitrage, covered properly below.

The venues, as they stand in mid-2026

Polymarket remains the liquidity center of gravity — a central limit order book settled in USDC on Polygon, plus (new in 2026) a separate CFTC-licensed US exchange following the QCEX acquisition. For arbitrageurs, Polymarket is usually one leg of any pair worth doing, because its depth lets you fill size with less slippage. We benchmark our own boxes against its live order book monthly-to-quarterly with a public script; the current measured numbers appear in the latency section.

Kalshi is a CFTC-regulated US exchange with a user base and market mix (policy, macro, finance) that diverges from Polymarket’s — and divergent participants are exactly where cross-venue gaps come from. Its fee formula is published and price-dependent (details below). Check current account eligibility for your jurisdiction directly with Kalshi; access rules have shifted over time.

Limitless, Myriad, Opinion are the thinner venues on the scanners — and thin liquidity is why their visible gaps run wider and close slower. The Ballon d’Or example above involved Myriad. The discipline: a wide spread on a thin book is an invitation to check depth, not to size up. Our platforms ranking compares them in detail.

Finding gaps: scanners are candidate generators, not signals

0xinsider’s arbitrage scanner watches all five venues and lists every pair trading under $1 — on May 26, 2026 it showed 598 live candidates. Treat each one as a lead to verify, on three checks, before any order goes out:

- Depth. The headline price is for the first contracts at the top of the book, not your full size. A 36¢ spread backed by 20 contracts is a 20-contract trade; reaching deeper repriced the rest. Read the book, size to what actually rests there.

- Fees. Scanners show gross spreads. Run the real fee math (next section) for your legs at your prices — at mid prices a small gross spread can vanish entirely into two taker fees.

- Age of the gap. A wide gap that has sat visible for half an hour is telling you something — usually thin books or a resolution-criteria difference. A small gap that just appeared is a race, and races are won by whoever is fastest (also next section).

0xinsider’s own guidance, paraphrased: fire both legs together, size to top-of-book, and use limit orders at or inside the best price rather than paying through the spread.

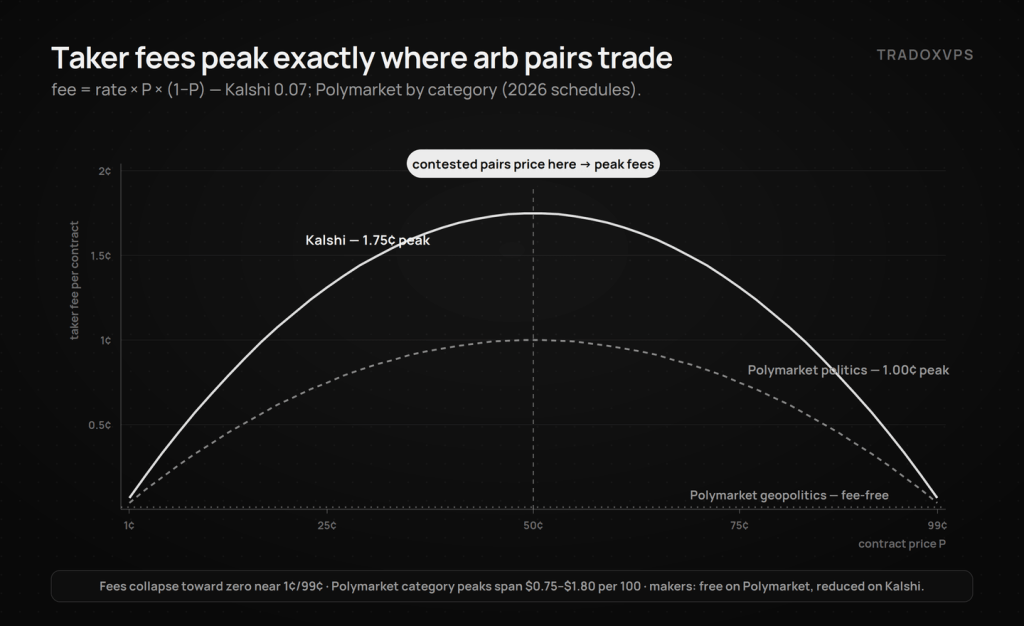

What actually eats your spread — with the 2026 fee formulas

Both major venues now price taker fees on a curve that peaks exactly where contested arb pairs live: 50¢.

Polymarket (international book), Fee Structure V2 — effective March 30, 2026. Taker fee per share = category rate × P × (1−P). Peak fees at 50¢ run from $0.75 per 100 shares on sports through $1.00 (politics, finance, tech) and $1.25 (economics, culture, weather) up to $1.80 on crypto — while geopolitics and world-events markets are fee-free. Makers pay zero, and collected taker fees fund daily maker rebates. The separate Polymarket US exchange has its own simpler schedule with a maker rebate. Always confirm against the official pages before modeling a trade: Polymarket’s trading-fees article and docs.polymarket.us/fees.

Kalshi. Taker fee per contract = 0.07 × P × (1−P) — a parabola peaking at 1.75¢ per contract at 50¢ and falling toward fractions of a cent near the extremes; maker orders are charged a fraction of the taker rate. Some series carry their own quirks, so verify on Kalshi’s published fee schedule.

Now the part that separates a real arb desk from a scanner tourist — the pair fee math. Take a contested event near 50/50: YES on Kalshi at 48¢, NO on Polymarket (politics category) at 49¢. Pair cost 97¢, gross spread 3¢. Fees if both legs are taker: Kalshi 0.07 × 0.48 × 0.52 ≈ 1.75¢; Polymarket 0.04 × 0.49 × 0.51 ≈ 1.00¢. Total 2.75¢ — your 3¢ spread nets a quarter of a cent before slippage. The same trade with the Polymarket leg posted as a maker order (fee: zero) nets 1.25¢ — five times more. And the same structure in a fee-free geopolitics market keeps 1.25¢ with no maker patience required on that leg.

Three structural conclusions fall out of the formulas: post maker legs wherever the gap’s lifespan allows it; fee pressure is lowest at extreme prices (both curves collapse toward zero near 1¢/99¢) and highest exactly at 50/50; and category choice is a fee decision, not just a liquidity one.

Slippage stacks on top: your realized average fill across a thin book is worse than top-of-book, and on size it’s often the binding constraint — bigger than fees. Execution risk is the third eater, and the most dangerous: between leg one filling and leg two filling, you hold an outright position. Submit both legs together where the venue allows, and never size a pair beyond what you could stomach holding one-legged through an adverse move.

Latency, honestly: what’s physics, what’s engineering, what’s marketing

You’ll see infrastructure vendors — historically including an older version of this very page — claim “1 ms to Polymarket.” We benchmarked that claim out of existence ourselves. In our June 2026 four-provider benchmark (one purchased box per provider, same public probe, raw JSON downloadable), Dublin boxes saw Polymarket’s live feed at ~13–15 ms median and round-tripped the order book warm at ~21–23 ms median. Nobody measured anything close to 1 ms, including us. Sub-millisecond claims to a CDN-fronted API are marketing; treat any vendor making them — about any venue — accordingly.

What latency actually buys an arbitrageur is position in a race. A fresh gap is a fixed pool of resting contracts that every bot watching both books is converging on. Lower latency means you observe the book change sooner and your order lands sooner; in a race for finite liquidity, ties go to the fastest. Three measured facts shape how to think about it:

- Medians are physics; races are won in tails. Across the four Dublin boxes we tested, order-path medians differed by barely a millisecond — but p99s ranged from 37 ms to 55 ms. The box that never exceeded 41 ms in 92 round-trips wins races that the box spiking to 86 ms loses, even though their medians look identical on a sales page.

- Geography is a floor no provider removes. An order from the US East Coast to Dublin pays the Atlantic crossing — tens of milliseconds of round-trip physics before any engineering happens. Same-metro execution doesn’t make you fast; it removes a handicap.

- The venue has tails too. Polymarket’s own API root showed a 250–650 ms p99 server-side tail on all four boxes we tested — identical everywhere, so it’s theirs, not the boxes’. Lesson for two-leg execution: “simultaneous” submission must tolerate venue-side stalls; that’s a sizing rule, not a latency purchase.

And one finding from our own data that matters specifically to cross-venue traders: routing is per-venue, per-box. Our Dublin box reached Polymarket fast — and its reference probe to Binance’s API routed to a far CDN edge at ~313 ms while three competitor boxes hit a near edge at ~208 ms. Same city, different routes. If your strategy prices one venue off another, measure every venue from the exact box you’ll trade it from; we publish the script, and yes, it caught our own weakness — which is on our routing desk and will be re-verified in the next public benchmark.

Risks the scanner never shows

Resolution divergence. Polymarket resolves via UMA’s optimistic oracle; Kalshi resolves under its regulated rulebook. On clean events they agree; on ambiguous ones they occasionally don’t — and a “hedged” pair that resolves differently on each venue becomes two outright positions. Low frequency, high impact: prefer markets whose resolution criteria are mechanical, and read both venues’ criteria, not just the titles.

Capital lock-up. Arb profit realizes at resolution. The honest yardstick is annualized: r = spread ÷ pair cost, annualized ≈ (1+r)^(365/days) − 1. An 8¢ spread on a 92¢ pair resolving in 90 days is ~8.7% absolute but ~40% annualized — attractive; the same spread locked for a year is a different trade. Professionals optimize capital velocity — turnover × average net spread — not headline spread size.

Liquidity withdrawal. Market makers can pull quotes faster than you can click. Depth at scanner-time is not depth at execution-time; size to the book you can see now, and expect it to be smaller when your order arrives.

For the broader strategic context around these markets, see how to win on Polymarket in 2026 and our Polymarket vs Kalshi comparison.

Infrastructure: what an arb operation actually needs

The practical dividing line: manual arb on wide, slow gaps needs a browser; automated arb on narrow, fast gaps needs always-on, low-tail infrastructure. If you’re hand-trading 10¢+ spreads on thin venues with long windows, a laptop is fine. If you’re competing for 1–3¢ gaps in liquid markets, you’re racing bots, and the requirements are concrete:

- Always-on execution. A home PC sleeps, updates, and drops Wi-Fi — each one a one-legged position waiting to happen. The full argument is in local PC vs VPS and the 24/7 bot guide.

- A short, measured path to each venue you trade. Not claimed — measured, from your box, with the 20-minute probe. Our Dublin boxes’ current numbers are published with raw data in the benchmark; for Kalshi-side execution, our Chicago location serves US-market traders (measure your own path there too — we don’t quote numbers we haven’t published).

- Enough box for multiple WebSocket books. A single-pair bot runs comfortably on our $44.90 Starter (2 cores, 6 GB); multi-venue scanning across five platforms wants the next tiers. The full sizing logic — what each resource does and what breaks first — is in the VPS specs guide.

- Software that fires both legs together and survives disconnects: WebSocket book mirrors per venue, pair-cost math in the hot loop, simultaneous order submission, and reconnect-and-resync logic so a dropped feed never trades on a stale book.

The honest test before paying anyone — including us: run the probe on a free 3-day demo, read your own tail numbers, and only then decide whether the race you’re entering needs them.

Frequently Asked Questions

Buying YES on one platform and NO on another for the same event at a combined cost under $1. Since exactly one side pays $1 at resolution, the difference is locked in regardless of outcome. It works because Polymarket, Kalshi, and smaller venues run independent order books that drift out of sync.

The resolved math is riskless if both legs fill at the modeled prices and both venues resolve identically. In practice you carry execution risk (one leg fills, the other moves), slippage beyond top-of-book, fee erosion (two taker legs near 50¢ can consume a 3¢ spread almost entirely under 2026 fee formulas), resolution divergence on ambiguous events, and weeks of capital lock-up.

Both major venues charge taker fees on a curve peaking at 50¢: Kalshi at 0.07 × P × (1−P) per contract (max 1.75¢), Polymarket by category from fee-free (geopolitics) up to a $1.80-per-100-shares peak (crypto), with maker orders free. A both-legs-taker pair at mid prices can pay ~2.75¢ — which is why serious arb posts maker legs and favors fee-light categories. Verify on each platform’s official fee page before trading.

Not for manual trades on wide, persistent spreads. For automated arb on narrow gaps, an always-on box with a short measured path to the venues is the difference between catching liquidity and arriving at an empty book. Judge any infrastructure — ours included — on published, reproducible measurements, not advertised milliseconds: our current numbers and the test script are public.

A cross-venue scanner like 0xinsider for candidates; venue APIs (Polymarket’s CLOB REST + WebSocket, Kalshi’s API) for book mirrors and execution; and a bot framework that verifies depth, runs the fee formulas, and submits both legs together. The scanner finds the lead; depth, fees, and speed decide whether it was real.

Fee structures verified June 2026 against the platforms’ published schedules; they change — always confirm before trading. Latency figures from our June 2026 Dublin benchmark (raw data public). We operate TradoxVPS and provide infrastructure, not financial advice; arbitrage involves real execution, resolution, and lock-up risks. Nothing here guarantees profit.