The conversation around NinjaTrader strategies has shifted in 2026. It is no longer primarily about what strategy you run — it is about whether your infrastructure can execute that strategy without cost. Every profitable approach discussed in this guide shares one common dependency: the ability to translate a signal into a filled order with zero operational overhead. Latency, uptime, and execution consistency are now part of the strategy itself.

This guide covers the most effective NinjaTrader strategies that active futures traders are deploying in 2026, with a hard focus on the execution realities that separate theoretical edge from realized P&L. If you are looking for surface-level indicator stacks and entry signals, this is not that article. What follows is a practitioner-level breakdown of strategy architecture, market conditions, NinjaScript implementation considerations, and the infrastructure prerequisites that determine whether each approach survives contact with live markets.

Why 2026 Demands a Different Approach to NinjaTrader Strategy

NinjaTrader has always been a serious platform for serious traders — NinjaScript-based automation, depth-of-market tools, native Rithmic and CQG connectivity, and a backtesting engine that remains one of the most rigorous in the retail space. But the trading environment it operates in has changed materially.

In 2026, futures markets — particularly CME products like ES, NQ, RTY, CL, and ZB — are increasingly shaped by three structural forces:

- Algorithm saturation at the micro level: Patterns that worked on 5-minute charts three years ago have been systematically arbed out by HFT and statistical arbitrage firms. Retail edge now requires either faster execution, better entry precision, or a structural approach that avoids competing directly with institutional algos.

- Volatility clustering: Macro uncertainty — driven by ongoing central bank policy cycles, geopolitical fragmentation, and commodity supply constraints — has led to sharper intraday volatility spikes. Strategies that are not designed for rapid regime shifts incur outsized drawdowns before they can adapt.

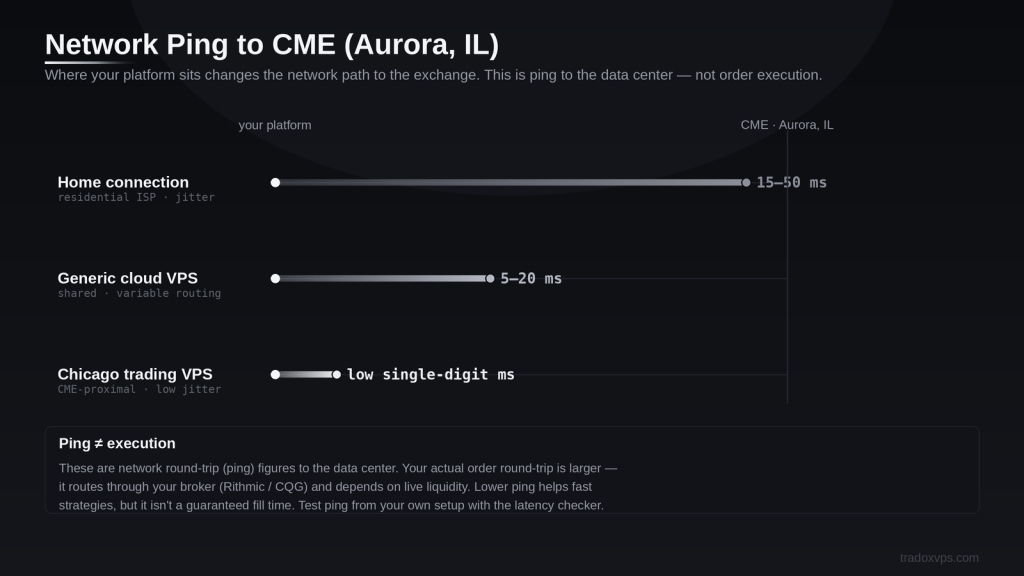

- Network path as a P&L variable: On fast strategies like scalping and breakouts, a data feed that reaches you in low single-digit milliseconds instead of tens of milliseconds shows up in fill quality. Note that these figures are network transit time (ping) to the data center — not full order-execution time, which also runs through your broker and depends on current liquidity.

The strategies that are working in this environment share a common profile: they are rules-based, infrastructure-aware, and built with execution cost (latency + slippage + commission) baked into the expected value calculation — not treated as an afterthought.

Below is a breakdown of the seven most effective NinjaTrader strategy archetypes active traders are running in 2026, followed by a detailed examination of the execution infrastructure requirements each one demands.

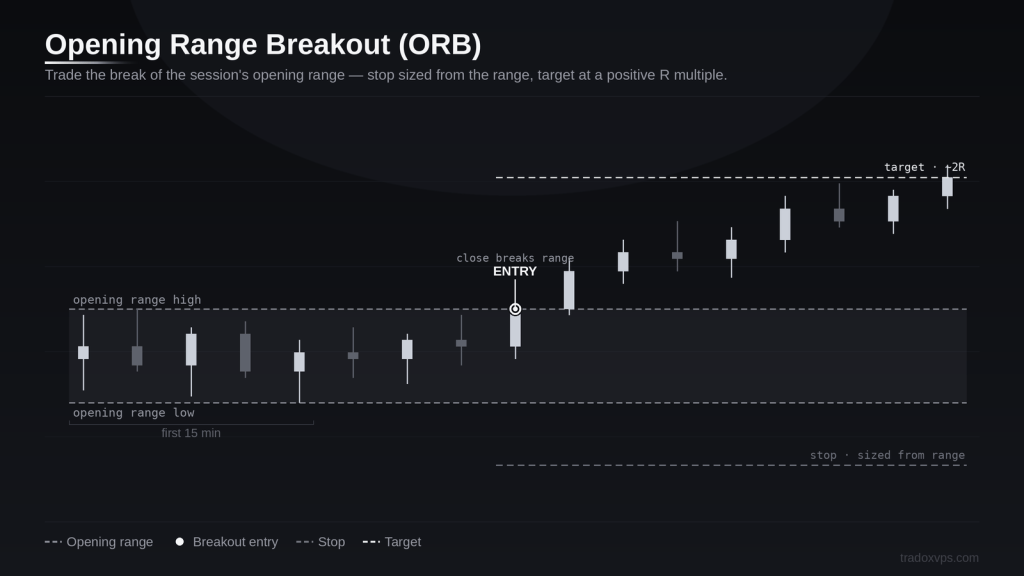

Opening Range Breakout (ORB) Strategy

What It Is and Why It Still Works

The Opening Range Breakout is one of the oldest systematic strategies in futures trading, and it remains one of the most structurally sound. Its persistence is not accidental — it is grounded in market microstructure. The first 5 to 30 minutes of the CME session (typically 9:30–9:35, 9:30–9:45, or 9:30–10:00 ET depending on the variant) represent the highest-information period of the trading day. Overnight positions are being squared. Economic data releases (CPI, NFP, FOMC) are being absorbed. Institutional desks are deploying capital based on pre-market analysis.

The price range established during this window reflects the market’s initial attempt to find equilibrium after incorporating all of this information. When price breaks decisively above or below this range, it signals that one side has dominated and momentum is likely to continue in that direction. This is not a lagging indicator pattern — it is a real-time read of order flow behavior.

Technical Implementation in NinjaTrader

In NinjaScript, the ORB is implemented by storing the high and low of the opening candles (or first N bars) as reference levels and then triggering entries when subsequent price action exceeds those levels. The typical implementation includes:

- Range definition window: The first 5, 15, or 30 minutes post-open. Shorter windows produce more signals with lower win rates; longer windows produce fewer but higher-quality signals.

- Breakout confirmation logic: Many robust implementations require a close above/below the range (not just a wick breach) to reduce false signals from wick fakeouts at the open.

- Volume filter: Requiring above-average volume at breakout to confirm institutional participation. In NinjaScript, this is implemented via the Volume indicator compared to a rolling average.

- Time filter: Blocking re-entries after a specific time (e.g., 11:30 ET) when morning momentum typically fades and price behavior becomes more random.

Execution Sensitivity

ORB is acutely sensitive to execution speed during the breakout moment. Because other systematic traders are watching the same price levels, the milliseconds immediately following a confirmed breakout are competitive. On a local machine with 15–40ms of network latency to the Chicago data center, you are systematically entering after faster participants. On a Chicago-based NinjaTrader VPS, your data and orders travel a far shorter network path — low single-digit milliseconds of ping to the CME’s Aurora data center — so you act much closer to the signal. (That ping is the time on the wire, not a guaranteed fill time; your broker and liquidity still set the final execution.)

| Infrastructure | Typical ping to CME data center | Entry Price Risk | Uptime Risk |

|---|---|---|---|

| Home PC (local ISP) | 15–50ms | High — consistent late entry | High — home internet, power |

| Generic cloud VPS | 5–20ms | Moderate | Moderate — shared resource contention |

| Chicago-based trading VPS | 0.5–2ms | Low — near-signal entry | Low — 99.999% SLA infrastructure |

These figures are network ping (round-trip) to the CME’s Aurora data center, not order-execution times. Real fills also route through your broker (Rithmic/CQG) and depend on liquidity.

Key Configuration Parameters

The most common performance-killer in ORB implementations is an undersized stop relative to the opening range width. If the opening range is 8 points on ES and the stop is set at 4 points, mean reversion during the breakout extension will repeatedly stop out positions that were directionally correct. A structurally sound ORB uses a stop derived from the range itself — typically 50–100% of the opening range width — and a profit target that provides a positive risk-to-reward ratio, often 1.5R to 2.5R depending on the timeframe.

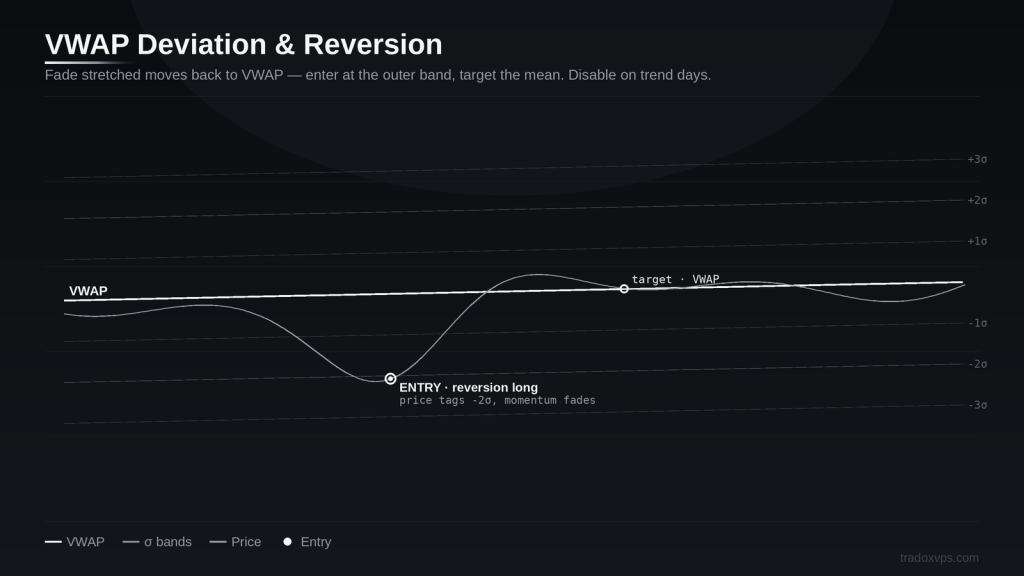

VWAP Deviation & Reversion Strategy

The Institutional Anchor Effect

VWAP (Volume Weighted Average Price) is one of the few indicators that has genuine institutional relevance — it is a benchmark used by large-order desk algorithms to measure execution quality. This creates a self-fulfilling structural property: institutional participants are programmatically buying below VWAP and selling above it during accumulation and distribution phases, which anchors price back toward the mean when it deviates excessively.

In 2026, VWAP-based reversion strategies have remained robust precisely because they are not dependent on momentum — they are dependent on the structural behavior of institutional order management. That behavior has not changed.

Strategy Architecture

The core logic is straightforward: when price deviates from VWAP by a statistically meaningful amount (typically measured in standard deviations, using bands similar to Bollinger Bands but anchored to VWAP), the probability of reversion increases. The implementation in NinjaTrader uses VWAP with standard deviation bands (1, 2, and 3 SD bands):

- Entry zone: Price reaches the 2nd or 3rd standard deviation band with momentum divergence — declining volume and a shrinking rate of price change.

- Entry trigger: A confirmed reversal candle (engulfing, pin bar, or inside bar breakout in the reversion direction).

- Target: VWAP itself, or the 1SD band on the opposite side if momentum is strong.

- Stop: Beyond the extreme of the deviation move, protecting against the strategy operating in a trending day where VWAP deviation can persist or expand.

Regime Awareness Is Critical

VWAP reversion fails systematically on trending days — days when price walks away from VWAP and never comes back. The highest-performing implementations include an ADX or range filter that disables the strategy when the market is in a strong trend. In NinjaScript, this means adding a condition: if ADX(14) > 30 and price is already extended, skip entries. This one filter can dramatically improve the strategy’s Sharpe ratio by reducing drawdown during adverse conditions without materially reducing trade count.

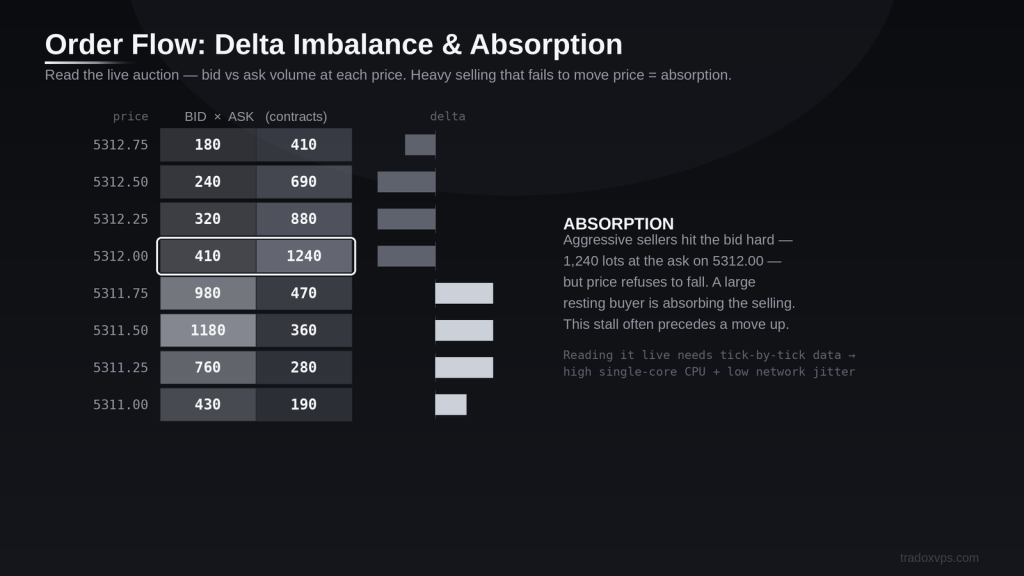

Order Flow Imbalance Strategy

Reading the Tape in 2026

Order flow analysis has become a distinguishing factor for serious futures traders in 2026. While chart-based indicators operate on processed, lagging data (closing prices, moving averages, oscillators), order flow reads the live auction as it happens — the actual bids being hit, offers being lifted, and the imbalance between market buy and market sell pressure at each price level.

NinjaTrader’s native DOM (Depth of Market) and its integration with tools like Bookmap (via NinjaTrader add-on), Sierra Chart connectivity, or the platform’s own footprint charts give traders direct access to this data. The footprint chart — which shows volume transacted at the bid versus the ask for each price level within a candle — is the primary analytical tool for this approach.

What You Are Looking For

The core concept is delta imbalance: a significant discrepancy between buy-side and sell-side volume at specific price levels. When price tests a level and aggressive selling (large delta negative) occurs but price does not move lower, it indicates absorption — a large buyer is taking the other side. This is often a precursor to a directional move in the buyer’s direction.

Specific setups include:

- Absorption at key levels: Heavy sell volume at a prior support/resistance level that fails to push price through — buyers are absorbing aggressively.

- Exhaustion prints: Extreme positive or negative delta at the end of a trend move, indicating the last wave of aggressive participants has been matched and the move is likely spent.

- Bid/ask stacking: In the DOM, large iceberg orders or consistent refreshing at a price level indicate a large participant defending that level.

NinjaTrader Implementation Notes

Order flow strategies are among the most data-intensive on NinjaTrader. They require tick-by-tick data processing (not bar data), which increases CPU and memory utilization significantly. A strategy running tick resolution data across 3–5 instruments simultaneously on a low-spec VPS will exhibit processing lag — the equivalent of software latency added on top of network latency. This is why order flow strategies specifically require high single-core CPU performance. NinjaTrader processes its core logic predominantly on a single thread, making clock speed more important than core count for this application.

| Strategy Type | Data Resolution | CPU Demand | RAM Demand | Latency Sensitivity |

|---|---|---|---|---|

| Opening Range Breakout | 1-minute bars | Low | Low (8GB sufficient) | High (entry timing critical) |

| VWAP Reversion | Tick/minute hybrid | Moderate | Moderate (16GB recommended) | Moderate |

| Order Flow Imbalance | Tick-by-tick | Very High | High (24GB+ recommended) | Very High |

| EMA Trend Following | Daily/hourly bars | Low | Low | Low–Moderate |

| Mean Reversion | 15-min/hourly bars | Low–Moderate | Moderate | Moderate |

| Scalping | Tick-by-tick | Very High | High (24GB+ recommended) | Extreme |

| Fully Automated Multi-Strategy | Mixed | Very High | Very High (32GB+) | High across all |

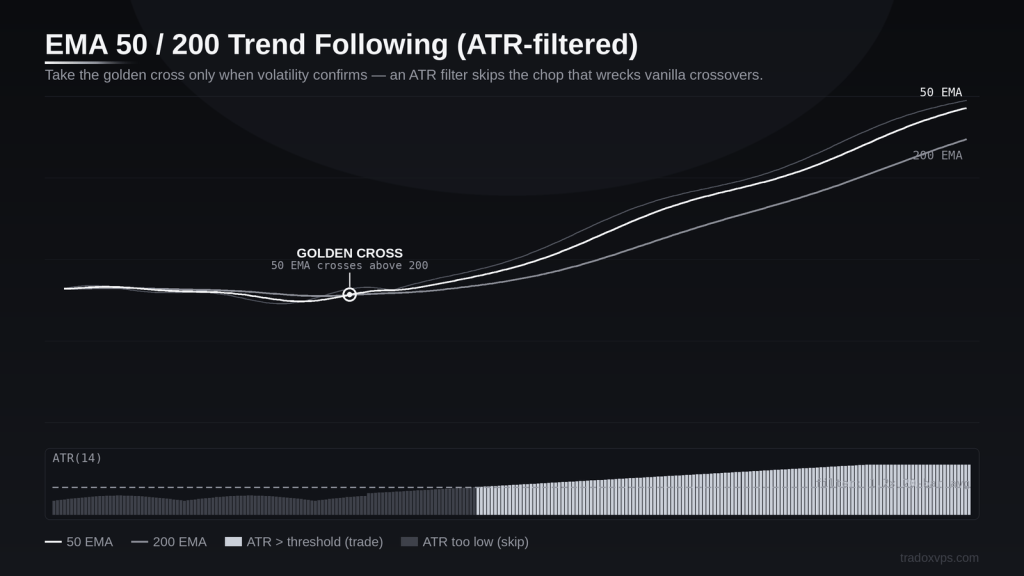

EMA-Based Trend Following with ATR Filters

Why Trend Following Survives Every Cycle

Trend following has one of the most durable track records in systematic futures trading, spanning decades of live performance across multiple market cycles. Its durability is structural: it profits from the persistence of directional price movement driven by macroeconomic forces that operate on timescales beyond the reach of noise traders.

In 2026, the environments most favorable to trend following have included commodity markets (energy, metals, agricultural), fixed income futures during rate policy pivots, and equity index futures during sustained institutional accumulation or distribution phases.

The 50/200 EMA Framework and Its Limitations

The classic implementation uses the 50 and 200 EMA crossover on daily or 4-hour charts as the primary signal. Long when the 50 EMA crosses above the 200 EMA (golden cross), short when it crosses below (death cross). While elegant in concept, this vanilla implementation suffers from one critical flaw: it generates late entries and produces false signals during choppy, sideways markets — which in 2026 represent a larger-than-historical proportion of market conditions due to central bank intervention cycles creating compressed ranges.

The modifications that make this work in 2026:

- ATR filter: Only enter when the current ATR(14) is above a minimum threshold relative to its 20-period average. This prevents entering during compressed ranges where trend continuation is unlikely. In NinjaScript:

if (ATR(14)[0] > SMA(ATR(14), 20)[0] * 1.2)— only allow entry when current volatility is at least 20% above its recent average. - Multiple timeframe confirmation: Require alignment on both the primary and one higher timeframe. A 4-hour crossover that conflicts with a bearish daily structure should be skipped.

- Trailing stop mechanism: Instead of fixed profit targets, use ATR-based trailing stops (e.g., 2.5× ATR below the highest close during the trade) to allow the strategy to capture extended trend moves rather than capping gains prematurely.

Position Sizing for Trend Following

Trend following strategies have lower win rates by nature — typically 35–45% — but their edge comes from asymmetric payoffs: losses are small and controlled, winners are multiples of the risk taken. This means position sizing is critical. Fixed-fractional sizing (risking 1–2% of account equity per trade, with position size determined by the distance to the stop in ATR terms) is the standard approach that allows the strategy to survive the inevitable losing streaks while remaining solvent to capture the large wins.

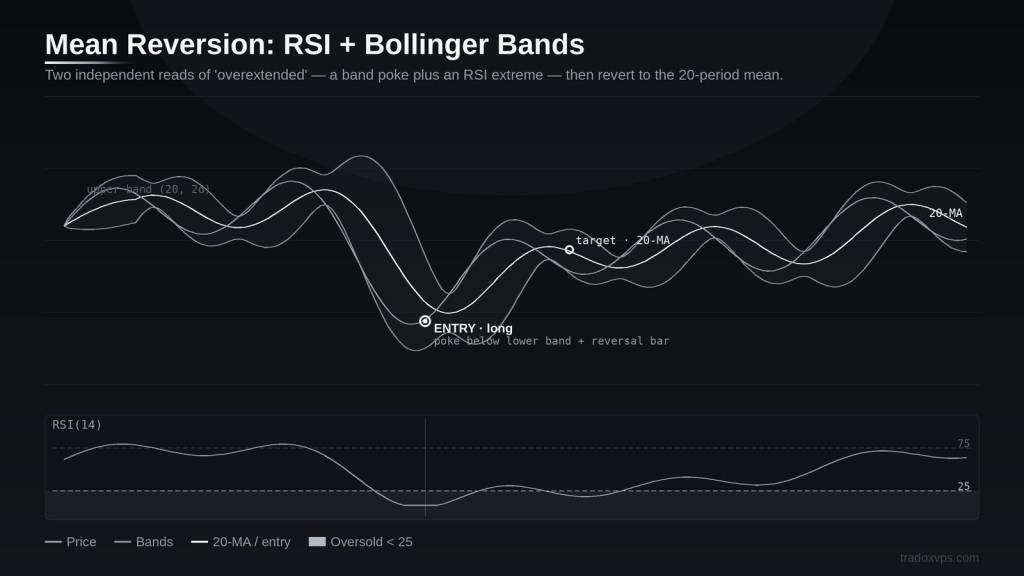

Mean Reversion in Defined Market Structures

The Statistical Foundation

Mean reversion operates on the statistical property that prices tend to return toward their historical average after periods of excess. In futures markets, this manifests as the tendency for extended moves to attract counter-directional order flow — profit-taking from trend participants, value buyers or sellers entering, and algorithmic positioning against extreme deviations.

In 2026, mean reversion works best in specific, identifiable market structures: instruments trading in defined ranges bounded by well-established support and resistance (often identified as prior swing points, volume nodes from the TPO profile, or psychological round numbers), and during periods of macroeconomic stability between major catalyst events.

RSI + Bollinger Band Implementation

The standard implementation in NinjaScript combines two independent measurements of “overextension”:

- RSI(14) < 25 for oversold (long signal) or > 75 for overbought (short signal)

- Price touching or exceeding the 2nd Bollinger Band (20-period, 2SD) confirming the statistical deviation

- Entry trigger: A reversal bar in the direction of mean reversion — not just a touch of the band, but a confirmed change in short-term momentum

- Target: The 20-period moving average (middle Bollinger Band), representing a return to statistical mean

- Stop: Beyond the extreme of the extension move — defined, non-negotiable

The Trending Day Problem and How to Address It

Mean reversion’s primary failure mode is the trending day. When a market is in a strong trend with institutional momentum, RSI stays in overbought/oversold territory for extended periods and Bollinger Band touches simply mark continuation points, not reversals. Every mean reversion trader has experienced the strategy’s Achilles heel: perfect entry signal, wrong day type, catastrophic drawdown.

The operational fix is a daily trend filter: before allowing any mean reversion entries, check whether the previous day closed with strong directional characteristics (a large range day, closing in the upper or lower 25% of its range). If yes, suppress entries for the current session. This one condition, properly implemented in NinjaScript, meaningfully reduces drawdown without eliminating the strategy’s edge during legitimate ranging conditions.

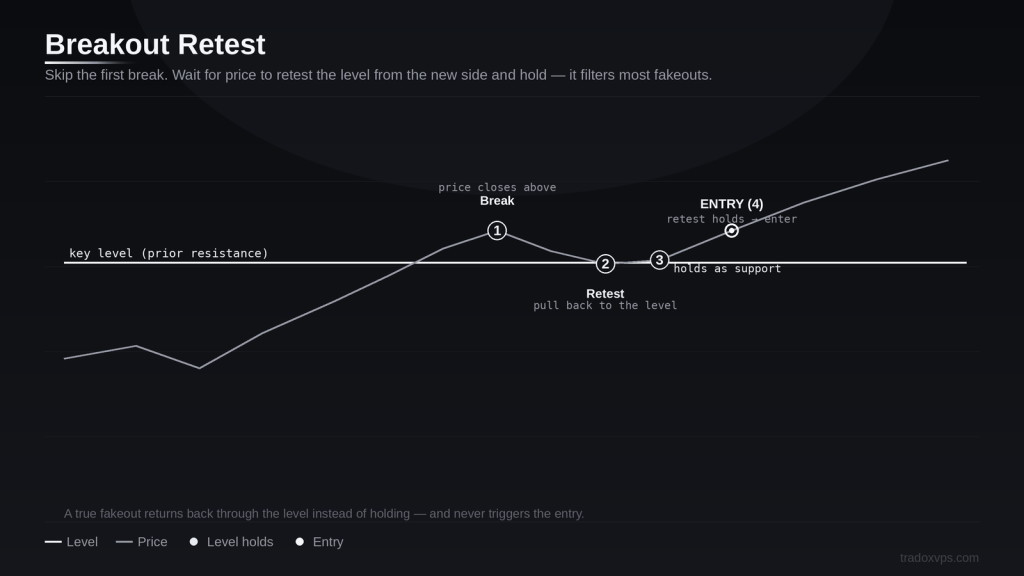

Breakout Retest Strategy

Why Pure Breakouts Fail and Retests Solve It

The pure breakout — buy the moment price closes above a key resistance level — was a viable strategy a decade ago. In 2026, it is systematically exploited. Algorithmic participants are programmed to push price above widely watched resistance levels, trigger retail stop orders and breakout entries, then reverse. This is not conspiracy — it is profit-seeking behavior by participants with better execution and more information than the average retail trader watching a level.

The retest strategy sidesteps this by introducing a confirmation requirement. The sequence becomes: (1) price breaks a key level, (2) price pulls back to retest that level from the new side, (3) the level holds (former resistance becomes support, former support becomes resistance), (4) a confirmed entry in the direction of the original breakout. This sequence filters out the majority of false breakouts because the fakeout pattern does not produce a successful retest — instead, price returns through the level and continues lower.

Identifying Valid Breakout Levels

Not all levels are equal. The highest-quality breakout/retest setups come from levels with specific characteristics:

- Multiple prior touches: A level tested 3+ times without breaking has a large number of resting orders associated with it. When it finally breaks, the follow-through tends to be substantial.

- Confluence with volume nodes: On a volume profile, price levels corresponding to high-volume nodes (HVN) and low-volume nodes (LVN) carry additional significance. LVNs above/below a breakout suggest the path of least resistance continues in the breakout direction.

- Alignment with higher timeframe structure: A level that is significant on both a 15-minute and hourly chart is more reliable than one visible only on the 5-minute chart.

NinjaTrader Automation Considerations

The breakout retest is one of the more challenging strategies to fully automate because the “retest quality” assessment involves judgment about the shape of the pullback, the time elapsed, and whether the level is holding. Partial automation — automating entry execution and risk management while leaving level identification and retest confirmation to the discretion of the trader — is the practical approach most algorithmic traders take in 2026.

Fully Automated NinjaScript Strategy Architecture

Building Strategies That Are Operationally Sound

Fully automated trading in NinjaTrader through NinjaScript represents the highest level of operational complexity — and the highest dependency on infrastructure reliability. When your strategy is running without human oversight, every operational failure mode becomes a trading risk.

A production-grade automated NinjaScript strategy in 2026 is not just about entry/exit logic. It is a system that includes:

- State management: The strategy must track its own state accurately — open positions, pending orders, daily loss limits. NinjaTrader’s native state machine (OnOrderUpdate, OnExecutionUpdate, OnPositionUpdate) must be implemented correctly or position tracking will drift from reality during high-activity periods.

- Daily loss limits: A hard cap on maximum daily losses, after which all positions are closed and no new entries are allowed. This is essential for strategies running without human oversight overnight.

- Connection loss handling: NinjaScript strategies need explicit handling for data feed disconnections. Without it, a disconnection followed by reconnection can leave the strategy in an undefined state — potentially with no active stop on an open position.

- Error logging: All order rejections, fill exceptions, and unexpected conditions should be logged with timestamps. This creates an audit trail that is invaluable when troubleshooting performance discrepancies between backtest and live results.

Multi-Strategy Portfolio Architecture

The most sophisticated NinjaTrader operators in 2026 are not running a single strategy — they are running a portfolio of uncorrelated strategies across multiple instruments, with correlation controls and portfolio-level risk limits applied dynamically.

This architecture requires significant compute resources. Each strategy instance consumes CPU cycles, memory for market data processing, and network bandwidth for order routing. Running 5–8 active strategies across ES, NQ, CL, ZB, and GC simultaneously on an underpowered VPS will produce resource contention that degrades all strategies’ execution quality. The requirement here is sufficient RAM (32GB or more) and multiple CPU cores with high single-thread performance.

NinjaScript Performance Optimization

There are specific development practices that significantly improve the runtime performance of NinjaScript strategies:

- Cache indicator values in local variables rather than calling the indicator object on each bar update — indicator method calls have overhead.

- Use

Calculate.OnPriceChangeonly when necessary;Calculate.OnBarCloseis significantly less CPU-intensive for bar-based strategies. - Avoid complex LINQ queries or heavy object instantiation in the

OnBarUpdatemethod — this runs on every tick and should be as lightweight as possible. - Pre-allocate collections in

OnStateChangerather than instantiating them inOnBarUpdate.

Backtesting Discipline and Walk-Forward Validation

Why Most Backtests Lie

The most common cause of live performance diverging from backtested results is not bad strategy logic — it is bad backtesting practice. In 2026, with access to NinjaTrader’s Strategy Analyzer and a growing ecosystem of third-party optimization tools, it has never been easier to curve-fit a strategy to look perfect on historical data and genuinely devastating in live markets.

The specific failure modes:

- Look-ahead bias: Using the close of a bar to trigger an entry that executes at the same bar’s close is physically impossible in live trading. The entry must be on the next bar’s open at minimum. NinjaScript’s

EnterLong()default behavior already accounts for this when usingCalculate.OnBarClose, but custom entry logic can inadvertently introduce look-ahead. - Commission and slippage omission: For scalping strategies operating on small per-trade targets (2–4 ticks on ES, each worth $12.50), commission of $4–5 round-trip and even 1-tick slippage per trade can eliminate the entire edge. A backtest without realistic execution cost assumptions is fiction.

- Optimization overfitting: Optimizing strategy parameters across the full historical dataset and then reporting results on that same dataset is circular. The in-sample results will be spectacular and the live performance will not.

Walk-Forward Validation in NinjaTrader

The standard of practice for professional systematic traders is walk-forward optimization. NinjaTrader’s Strategy Analyzer includes a walk-forward module that automates this process. The methodology:

- Divide historical data into sequential segments — typically 70% in-sample and 30% out-of-sample.

- Optimize parameters on the in-sample window, apply the best parameters to the out-of-sample window, record results.

- Slide the window forward and repeat across the full dataset.

- Aggregate the out-of-sample results — this represents the closest approximation to live performance the backtesting process can produce.

A strategy that shows consistent out-of-sample performance across multiple walk-forward windows has demonstrated adaptive robustness. A strategy that only looks good in aggregate in-sample analysis is likely curve-fitted and will underperform in live markets.

Monte Carlo Simulation for Drawdown Analysis

Beyond walk-forward, Monte Carlo simulation applied to the sequence of trade outcomes gives a distribution of possible drawdown scenarios. If the Monte Carlo analysis at a 95th percentile confidence interval shows a maximum drawdown 3× larger than the historical maximum, the live risk exposure is substantially higher than the backtest suggests. This analysis should inform initial position sizing and daily loss limits before deploying any strategy to a live account.

The Hidden Cost That Destroys Edge

The Hidden Cost That Destroys Edge

Every strategy discussed in this guide has an expected value that assumes some level of execution quality. When that execution quality is degraded by infrastructure limitations — latency, processing lag, connectivity instability — the expected value decreases. For strategies operating on thin margins (scalping, ORB, order flow), the degradation can be sufficient to turn a profitable system unprofitable.

The specific mechanism is straightforward: execution delay maps directly to price impact. If your signal triggers at time T and your order reaches the broker tens of milliseconds later instead of a few, you are entering a market that has had extra time to move away from your target price. In a liquid instrument like ES, where the bid-ask spread is typically 1 tick ($12.50) and the market can move 0.25–0.5 points per second during high-activity periods, that delay can cost a few dollars of slippage per trade — and across hundreds of trades a year, the drag adds up. This is why shortening the network path between your platform and the exchange matters for fast strategies.

The Uptime Equation

For automated strategies running overnight or during extended sessions, uptime is a direct risk factor. Consider the scenario: your strategy has an open short position in CL (crude oil futures) overnight. At 2:47 AM, your home internet connection resets for a routine ISP maintenance window — 4 minutes of disconnection. Your NinjaTrader strategy loses its data feed connection. Without explicit connection-loss handling, the strategy may not recognize that it is disconnected. If price moves against the position during those 4 minutes, no stop order is active (or the stop was submitted and then rejected during the disconnection). The position accumulates unmanaged loss.

This is not a hypothetical — it is a documented failure mode that occurs regularly for traders relying on residential internet for live automated trading. A trading-grade VPS with 99.999% uptime and redundant network paths eliminates this risk class entirely.

Network: Geographic Proximity and Consistency

What “Optimized for Trading” Actually Means

Not all VPS providers are equivalent, and the marketing language around “trading VPS” is heavily diluted. What matters operationally for NinjaTrader performance is specific and measurable.

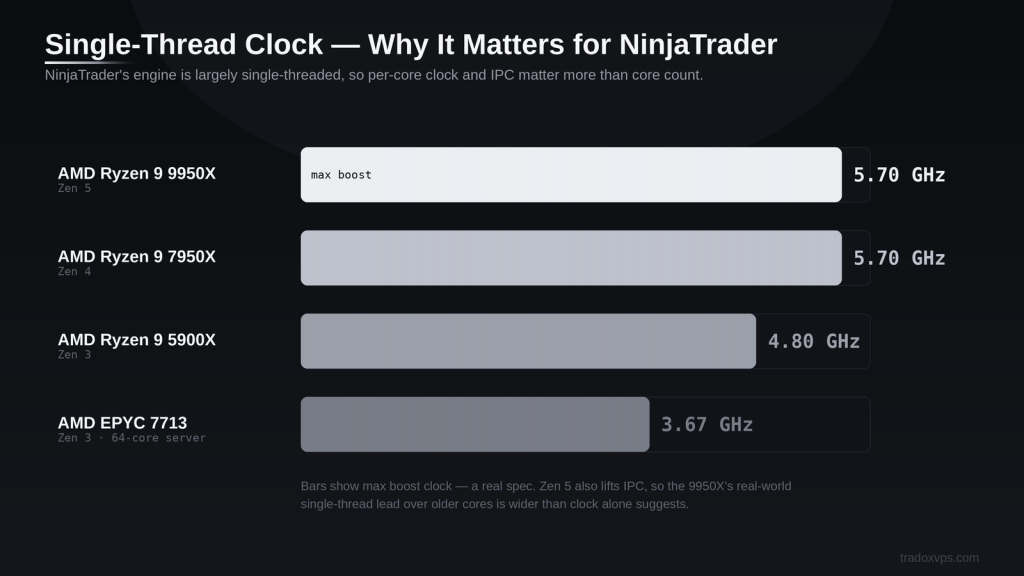

CPU Architecture: Single-Core Performance Over Core Count

NinjaTrader’s execution engine, order routing, and much of the NinjaScript runtime operate primarily on a single thread. This is a platform-level design characteristic that means single-core performance — specifically, single-thread speed measured by clock frequency and instructions-per-clock (IPC) — is more important than total core count for NinjaTrader specifically.

The AMD Ryzen 9 9950X (Zen 5 architecture) represents the current benchmark for single-thread trading performance in VPS environments. With base clocks at 4.3GHz and boost clocks reaching 5.7GHz, combined with Zen 5’s improved IPC versus prior generations, it delivers NinjaScript processing throughput that older server CPUs (EPYC 7713 at 2GHz base, for example) cannot match — regardless of how many EPYC cores are available.

| CPU | Architecture | Base / Boost Clock | Single-Thread Performance | NinjaTrader Suitability |

|---|---|---|---|---|

| AMD Ryzen 9 9950X | Zen 5 | 4.3GHz / 5.7GHz | Excellent | ⭐⭐⭐⭐⭐ Optimal |

| AMD Ryzen 9 7950X | Zen 4 | 4.5GHz / 5.7GHz | Very Good | ⭐⭐⭐⭐ Strong |

| AMD Ryzen 9 5900X | Zen 3 | 3.7GHz / 4.8GHz | Good | ⭐⭐⭐ Adequate |

| AMD EPYC 7713 | Zen 3 | 2.0GHz / 3.7GHz | Moderate (many cores, slow per-core) | ⭐⭐ Poor for single-thread workloads |

| Intel Xeon E5 (legacy) | Broadwell/Skylake | 2.2–3.5GHz | Low | ⭐ Not recommended |

Memory: DDR5 and Why It Matters for Tick Data

DDR5 memory offers roughly 1.5–2× the bandwidth of DDR4 at equivalent capacity. For NinjaTrader workflows processing high-resolution tick data across multiple instruments, memory bandwidth directly impacts the speed at which market data is moved from storage into the processing pipeline. This is not theoretical — under sustained tick-data load (as in order flow or scalping strategies), DDR4 systems show measurable processing latency increases compared to DDR5-equipped systems with identical CPU configurations.

Network: Geographic Proximity and Consistency

For CME futures (ES, NQ, RTY, CL, ZB, GC — the instruments most commonly traded through NinjaTrader), the exchange co-location is in Aurora, Illinois (CME Group’s primary data center). Network latency from Chicago-based data centers to this facility is physically constrained by the speed of light and fiber routing — typically achieving 0.5–2ms round-trip time. From New York, the best-case latency is 8–10ms. From a home network in a suburban area, 15–50ms is typical.

Beyond average latency, jitter (latency variance) matters equally for automated strategies. A system that averages 2ms latency but spikes to 45ms every few minutes will produce unpredictable fill quality that makes order flow strategies effectively non-functional during those spikes. Enterprise-grade network infrastructure, designed for financial market connectivity, maintains consistent latency with minimal jitter in a way that residential ISP connections cannot match.

Operating System and Platform Configuration

Windows Server 2022 (the standard OS for trading VPS deployments) provides several performance advantages over consumer Windows editions for NinjaTrader operation:

- Server-grade process scheduling: Prioritizes application threads more aggressively, reducing background process interference with NinjaTrader’s execution engine.

- Reduced background services: A properly configured trading VPS disables unnecessary Windows services (automatic updates during trading hours, Windows Defender real-time scanning of trading data files, superfetch/prefetch) that create CPU spikes at unpredictable intervals.

- Power plan configuration: High-Performance or Ultimate Performance power plans prevent CPU clock throttling, ensuring consistent single-core boost performance during strategy execution.

Strategy–Infrastructure Compatibility Matrix

Not every strategy has identical infrastructure requirements. The following matrix maps each strategy archetype to its minimum and recommended VPS specifications, helping traders right-size their infrastructure investment relative to their strategy’s actual needs.

| Strategy | Min RAM | Rec. RAM | CPU Cores (Rec.) | Latency Priority | Uptime Criticality | TradoxVPS Plan |

|---|---|---|---|---|---|---|

| Opening Range Breakout | 8GB | 16GB DDR5 | 2–4 | High | Moderate | Starter / Active |

| VWAP Reversion | 8GB | 16GB DDR5 | 4 | Moderate | Moderate | Active Trader |

| Order Flow Imbalance | 16GB | 24–32GB DDR5 | 6–8 | Very High | High | Advanced / High Performance |

| EMA Trend Following | 8GB | 16GB DDR5 | 2–4 | Low | High (overnight) | Starter / Active |

| Mean Reversion | 8GB | 16GB DDR5 | 4 | Moderate | Moderate | Active Trader |

| Breakout Retest | 8GB | 16GB DDR5 | 4 | Moderate–High | Moderate | Active Trader |

| Scalping (high-frequency) | 16GB | 32GB DDR5 | 6–8 | Extreme | Extreme | High Performance / Ultra |

| Multi-Strategy Automated | 24GB | 48–64GB DDR5 | 12–16 | High | Extreme | Ultra / Max Performance |

Data Feed Selection

Independent of VPS configuration, the choice of data feed has a direct impact on the quality of market data your NinjaTrader strategies receive. The two primary options for serious futures traders:

- Rithmic: The industry-standard data feed for CME futures, offering direct market access with typical feed latency in the microsecond range for co-located systems. The standard for professional and semi-professional automated traders.

- CQG: An alternative with strong institutional penetration and competitive latency. Compatible with major brokers including AMP Futures, Ironbeam, and others.

Kinetick (NinjaTrader’s native data feed) is adequate for discretionary and moderate-frequency automated trading, but serious latency-sensitive strategies should use Rithmic or CQG for the best available data quality and feed reliability.

Conclusion

The NinjaTrader strategies that are generating consistent results for futures traders in 2026 share a common architecture: they are rules-based, their edge is quantified and validated through rigorous backtesting, and they are designed with execution cost as a first-class variable in the expected value calculation — not an afterthought.

Opening Range Breakout, VWAP reversion, order flow imbalance, EMA trend following, mean reversion, breakout retest, and fully automated algorithmic systems each have defined roles in a trader’s arsenal, and each has specific conditions under which they perform well. The critical discipline is understanding those conditions and having the infrastructure stability to let the strategies execute as designed without operational interference.

What separates traders who achieve consistent live performance from those who see persistent divergence from their backtested results is rarely the quality of the strategy itself. It is almost always execution quality — latency, uptime, processing reliability, and data feed consistency. These are infrastructure problems, not strategy problems.

For NinjaTrader operators who are serious about trading CME futures systematically, the logical infrastructure choice is a Chicago-based NinjaTrader VPS with CME-proximal network connectivity, DDR5 memory, and a high single-core clock-speed CPU. This eliminates the infrastructure variables that degrade strategy performance and allows the underlying edge — however small — to accumulate consistently over time.

If you are running NinjaTrader strategies that are generating theoretical edge in backtesting but underperforming in live markets, before revising the strategy, audit your execution environment. The answer is often there.

Frequently Asked Questions

There is no universal “best” NinjaTrader strategy — effectiveness depends on market conditions, the trader’s risk tolerance, and capital allocation. In 2026, the most consistently profitable strategies are those combining robust rules-based logic with proper execution infrastructure. Opening Range Breakout and order flow imbalance strategies have strong risk-adjusted returns in liquid CME futures; fully automated multi-strategy portfolios offer the most scalable approach for serious systematic traders.

Network latency from your NinjaTrader platform to the CME exchange directly affects order fill quality. A Chicago-based VPS sits within low single-digit milliseconds (network ping) of the CME’s Aurora data center, compared to 15–50ms from a home connection — and that ping is the time on the wire, not the full order round-trip through your broker. For latency-sensitive strategies — scalping, opening range breakout, order flow — this difference maps directly to entry price quality and, over hundreds of trades, to realized P&L.

For a single automated strategy on one or two instruments, 8–16GB DDR5 RAM is adequate. For order flow strategies processing tick-by-tick data, or for running multiple simultaneous automated strategies across multiple instruments, 24–32GB is recommended. Full multi-strategy portfolio automation across 5+ instruments should be provisioned with 48GB or more to avoid memory pressure impacting processing latency.

Yes — this is the primary operational advantage of a trading-grade VPS over a home setup. A properly configured NinjaTrader deployment on a VPS with a 99.999% uptime target, redundant network connectivity, and automated reconnection logic will run continuously without intervention. Automated strategies can monitor overnight sessions, execute pre-market setups, and manage open positions during any trading hour without requiring the trader to be present.

For serious automated trading of CME futures, Rithmic is the industry standard data feed. It provides direct market access with institutional-grade feed reliability and minimal latency. CQG is a strong alternative with broad broker compatibility. Both are meaningfully superior to Kinetick for latency-sensitive automated strategies, though Kinetick remains adequate for discretionary and moderate-frequency systematic trading.

The primary causes of backtest-to-live divergence are: (1) insufficient slippage and commission modeling in the backtest, (2) look-ahead bias in entry logic, (3) curve-fitting strategy parameters to in-sample data without walk-forward validation, and (4) execution latency in the live environment degrading fill quality beyond what the backtest assumes. Address all four: use realistic execution cost assumptions, validate with walk-forward optimization, and run on low-latency VPS infrastructure that minimizes the live execution gap.

Scalping is viable but requires exceptional execution infrastructure. The profit-per-trade in scalping strategies is small — often 2–4 ticks on ES — which means commission, slippage, and latency consume a large portion of the theoretical edge. Retail scalping on NinjaTrader is most viable when running on a Chicago-based VPS with a short network path to the CME (low single-digit-millisecond ping), using a low-commission broker with Rithmic connectivity, and with NinjaScript strategy code optimized for minimal processing overhead on each tick update.

TradoxVPS is a Chicago-based trading VPS provider engineered specifically for futures and algorithmic traders. Powered by AMD Ryzen 9 9950X (Zen 5) processors, DDR5 RAM, NVMe SSD storage, and a Chicago network path positioned close to the CME’s Aurora data center, TradoxVPS is built to support the operational demands of serious NinjaTrader deployments — from single-strategy discretionary setups to fully automated multi-instrument portfolio systems. Learn more about TradoxVPS NinjaTrader VPS plans.