Writing the algorithm is the easy part. A moving-average crossover is about twenty lines of Python, and you could have it backtesting by tonight. What’s hard is everything the code quietly assumes: that your edge is real and not a coincidence, that the fills you saw in the backtest will show up in a live order book, and that your bot will still be online when the one trade that pays for the month finally prints.

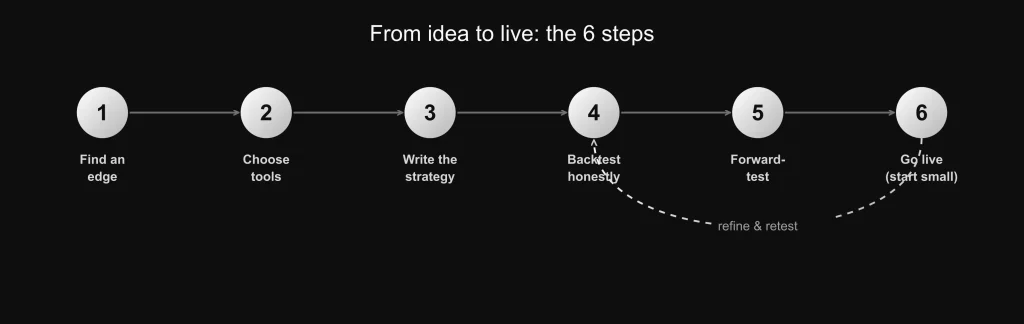

Most trading algorithms that look brilliant on a backtest never make money. They aren’t unlucky. They’re overfit, under-tested, or running on a machine that drops them at the worst possible moment. This is the full path from idea to live order, and it’s honest about where algorithms actually die.

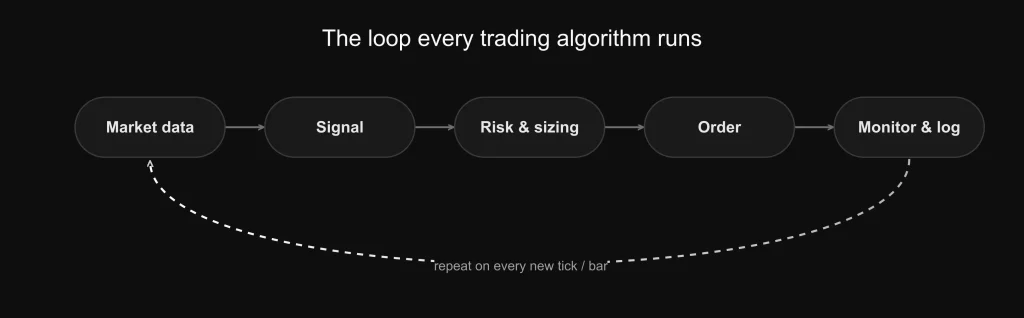

What a trading algorithm actually does

A trading algorithm is a program that turns market data into orders with no human pressing the button. Strip away the buzzwords and every one of them, from a two-line crossover to a deep-learning model, runs the same loop: read the market, decide, size the trade and check your risk limits, send the order, then log what happened and watch the position. The rules in the middle can be trivial or fiendishly complex. That part is not what makes money. Getting the loop to behave when real capital and a real exchange are involved is.

Step 1: Find an edge worth coding

The most common way to waste a month is to open a backtester and tweak parameters until the equity curve points up and to the right. That doesn’t find an edge. It finds the random noise in your sample and dresses it up as a strategy.

Work the other way around. Before you write a line of code, finish this sentence: “I think I can make money because ___, and that will keep working because ___.” If you can’t fill in both blanks, you don’t have a strategy yet. Most genuine edges come from one of a few places:

Trend-following rides moves that persist longer than people expect, using breakouts or moving averages. Mean-reversion does the opposite, fading prices that have stretched too far from a fair value — it prints money in choppy, range-bound markets and gives it all back in a strong trend, so knowing which regime you’re in matters more than the entry rule. Arbitrage exploits the same thing being priced two different ways; those gaps close in milliseconds, so it’s automation or nothing. Market-making earns the bid-ask spread by quoting both sides, which sounds like free money until you realize you get filled fastest exactly when the price is about to move against you. And then there’s plain informational edge: you understand a specific market, mechanism, or dataset better than the people pricing it.

Write your thesis down. It’s the thing you’ll test, and the thing that tells you when a strategy has quietly stopped working and it’s time to turn it off.

Step 2: Choose tools that are still alive in 2026

Three choices here: your language, your backtesting engine, and your data.

Language is the easy one. Python is the right answer for almost everyone — clean syntax, and the entire data-science ecosystem (Pandas, NumPy, scikit-learn) sits right next to it. You only need C++ or Rust if your edge genuinely lives in microseconds, which for retail it almost never does. If you’re committed to a specific platform you’ll use its language instead: NinjaScript (C#) for NinjaTrader, EasyLanguage for TradeStation, MQL4/5 for MetaTrader.

The backtesting engine is where people get burned, because the most-recommended library is a trap. Backtrader was the default for years and most tutorials still point to it, but it has been effectively unmaintained since around 2021 — no recent releases, and it now throws dependency and compatibility errors on current Python versions. It’s fine for learning from old forum posts; it’s a bad foundation for anything new. What’s actually maintained in 2026:

- Backtesting.py — the simplest to start with, clean API, readable results. Research only, no live trading. This is where a beginner should begin.

- VectorBT (free) or VectorBT PRO — vectorized and extremely fast, built for sweeping thousands of parameter combinations. The free version covers most research; PRO adds proper order-fill and intra-bar stop modeling.

- NautilusTrader — event-driven, built for production, with realistic order semantics and latency modeling. More engine than a beginner needs, but the one to grow into if you’re going live with real money.

- pysystemtrade if you’re doing systematic, risk-budgeted futures; Zipline-Reloaded if you’re doing equity factor research.

Data quality matters more than data quantity. A survivorship-biased universe, a handful of bad ticks, or a timezone mismatch will quietly invalidate an entire backtest and you’ll never know. Decide what resolution you actually need — tick data for fast strategies, minute or hourly bars for swing systems — and clean it before you trust a single result.

Step 3: Write the strategy

Keep the code in separate pieces so you can test and swap each one: a data handler that feeds in prices, the strategy logic that produces signals, a risk manager that sizes positions and enforces limits before anything goes out, an execution layer that places orders and tracks their fate, and a logger that records every decision so you can compare live results to expectations later.

The piece beginners skip is order handling. Your backtest assumes the order fills. Reality offers rejections, partial fills, and orders that sit there while the market walks away. Here’s a complete, current Backtesting.py example — a moving-average cross with commissions modeled — that shows the shape of a real strategy:

import pandas as pd

from backtesting import Backtest, Strategy

from backtesting.lib import crossover

def SMA(values, n):

"""Simple moving average over the last n bars."""

return pd.Series(values).rolling(n).mean()

class SmaCross(Strategy):

fast, slow = 20, 50 # the only two knobs — keep it that way

def init(self):

price = self.data.Close

self.ma_fast = self.I(SMA, price, self.fast)

self.ma_slow = self.I(SMA, price, self.slow)

def next(self):

if crossover(self.ma_fast, self.ma_slow):

self.buy() # bullish cross -> go long

elif crossover(self.ma_slow, self.ma_fast):

self.position.close() # bearish cross -> flatten

# data = a DataFrame with Open, High, Low, Close columns and a datetime index.

# commission=0.002 means 0.2% per trade — never run a backtest with zero costs.

bt = Backtest(data, SmaCross, cash=10_000, commission=0.002)

stats = bt.run()

print(stats)

Two habits are baked in there on purpose: it only carries two parameters, and it never sends a new order while it’s already in a position. Those two disciplines alone prevent a large share of the mistakes that blow up live accounts. One honest caveat about this tool: Backtesting.py is for research, and it doesn’t model slippage on its own. When you need realistic fills and latency, that’s VectorBT PRO or NautilusTrader territory.

Step 4: Backtest without fooling yourself

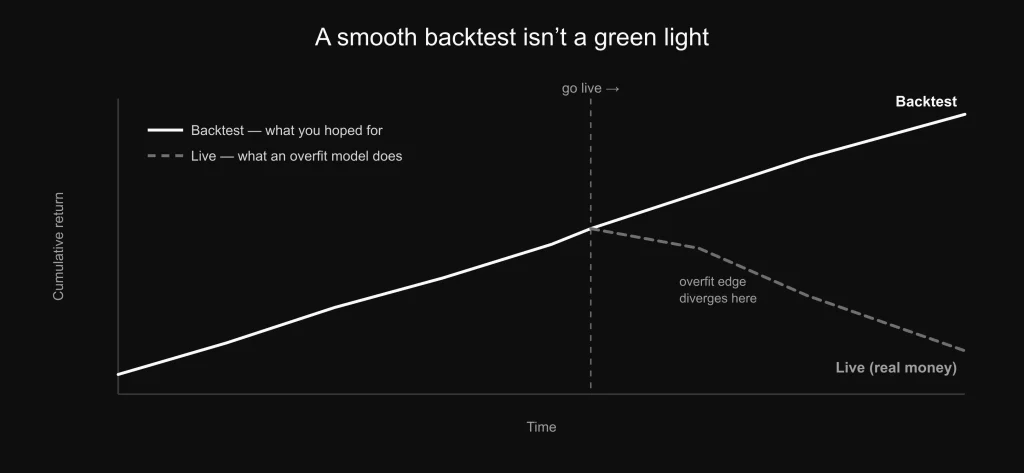

A backtest’s job is not to make you feel good. It’s to try to kill your strategy before the market does. The thing doing the killing is overfitting: tuning the algorithm so tightly to past data that nothing predictive is left.

A few rules make that harder to do by accident. Keep your parameter count low — three or four, not fifteen, because every extra knob is another way to fit noise, and running hundreds of backtests over the same data has the same effect (eventually something “works” purely by chance). Always test on data the strategy has never seen, and walk forward: fit on one window, test on the next, then roll the window. Charge realistic costs, then double your slippage estimate as a stress test; if the edge dies under that, it was never there. And try perturbing the historical prices slightly — if your profits evaporate when the data wiggles a little differently, you fit the wiggles, not a pattern.

Learn to read the warning signs. An equity curve that’s suspiciously smooth is a red flag, not a green one. A win rate north of 70% on a simple strategy usually means you’ve curve-fit. Performance that falls apart when you nudge one parameter means the result was fragile to begin with. Judge what survives on out-of-sample Sharpe ratio, maximum drawdown, and profit factor — and pay attention to how much those numbers degrade from in-sample to out-of-sample, because that gap is your honest estimate of how the thing will behave on money.

Step 5: Forward-test on live data

Surviving an honest backtest earns your strategy a forward test, not a funded account. Run it in a paper or evaluation account against live market data for one to three months. This is where the gap between backtest and reality shows up as actual numbers: fills you assumed at the midpoint that land at the bid or ask, the delay between your signal and your order that the backtest treated as zero, reconnects, data gaps, the occasional rejected order.

Remember that the simple research tools won’t trade live for you. Going live means connecting to your broker’s API directly or running a production framework like NautilusTrader that’s built for it. And if your paper results come in noticeably worse than the backtest, believe the paper results — your backtest was optimistic, and you fix that before risking a cent, not after.

Step 6: Go live with the brakes installed

When you finally switch on real money, start with size small enough that a losing streak is tuition, not a disaster. These controls are not optional: a defined stop on every trade, position sizing that risks a small fixed percentage of equity per trade, a daily loss limit and a kill switch that halts trading on its own, a maximum-drawdown circuit breaker, and reconnect-and-resync logic so a dropped connection never leaves a position flapping in the wind. Then watch live performance against what the backtest promised, and only scale up when the two actually agree.

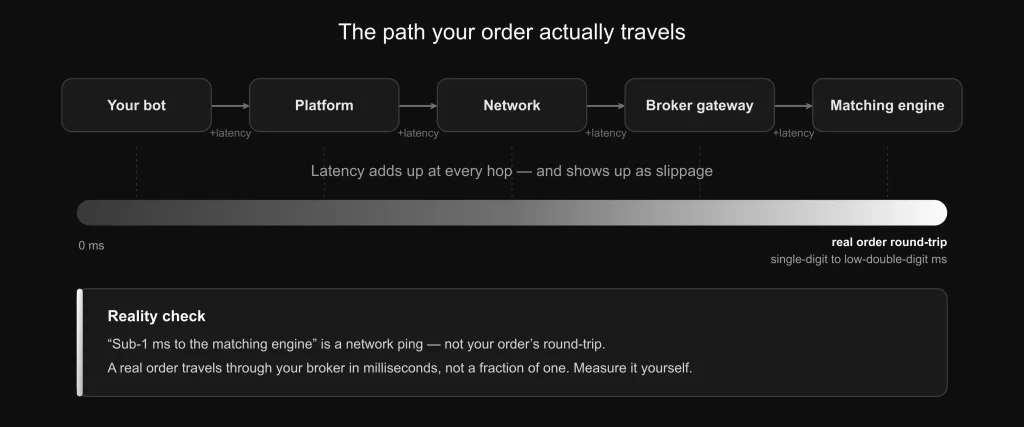

The part the tutorials skip: where your algorithm runs

Here’s the thing most guides never mention because they’re written by people who’ve never had to keep a bot online. Your backtest silently assumes instant, perfect, always-on execution. Live, every order takes a physical journey — your platform processes the signal, your network carries it, your broker’s gateway forwards it, the matching engine acts. Each one of those hops adds a few milliseconds, and those milliseconds show up in your P&L as slippage. That’s the quiet reason a profitable backtest underperforms live.

Four things decide whether your edge survives the trip.

It has to stay on. A laptop that goes to sleep, or a home connection that hiccups during a news spike, is a missed entry or a stale resting order with your money behind it. Anything time-sensitive or overnight belongs on a server that doesn’t sleep. (We lay out the honest trade-offs in trading VPS vs home PC.)

Single-core speed beats core count. The loop that reads a tick, decides, and signs an order is mostly single-threaded, so a high clock speed helps far more than a stack of slow cores. It’s why we run AMD Ryzen 9 9950X chips that boost to 5.7 GHz rather than the recycled many-core server CPUs a lot of hosts quietly use (why the 9950X, specifically). Give it room, too — a breaking event can multiply incoming message volume in seconds, and you don’t want a memory spike killing your bot mid-position (how much RAM you actually need).

And location helps, but only if you measure it instead of believing the ad. This is the part the industry lies about most: anyone advertising “sub-1ms to the matching engine” is quoting you a network ping, not an order round-trip. A real order traveling through a broker is single-digit to low-double-digit milliseconds, never a fraction of one. Don’t take that number on faith from anyone, us included — run a latency check from the actual machine to the actual venue before you pay for proximity, and here’s how we benchmark it honestly so you can do the same anywhere.

None of this matters for a slow, judgment-based strategy you trigger by hand — a clean laptop is plenty. It matters enormously for arbitrage, market-making, or news reaction, where the infrastructure is part of the strategy. A single-strategy bot runs comfortably on a modest plan; you can see current specs and pricing here.

The risks nobody puts in the headline

Automating a strategy doesn’t remove risk. It just lets a bad rule lose money faster than you can react. Overfitting is the one that gets most people — a strategy fitted to the past with no edge left for the future. Then there’s execution risk, where fills move and orders get rejected and the legs of a spread fill apart; data risk, where a dirty or biased dataset produces a backtest that was never true; and platform risk, because APIs, fees, and rules change, and a strategy built on last quarter’s parameters slowly stops working. The traders who last aren’t the ones with the cleverest models. They’re the ones who tested honestly, sized small, and respected every item on that list.

Frequently asked questions

Yes. Start with one simple, explainable strategy in Python and Backtesting.py. The skill that decides whether you make money isn’t fancy machine learning — it’s honest validation and disciplined risk control, and both are learnable.

Python for the overwhelming majority of strategies, thanks to its data and backtesting ecosystem. Reach for C++ or Rust only if you’re genuinely competing on microseconds. Use a platform’s native language (NinjaScript, EasyLanguage, MQL) if you’re tied to that platform.

It’s a great way to learn from its enormous archive of examples, but it has been effectively unmaintained since around 2021 and now has dependency issues on modern Python, so it’s a poor base for new systems. For new work, use Backtesting.py to start, VectorBT for fast parameter research, or NautilusTrader for live, production-grade execution.

Almost always two things together: overfitting (the strategy was tuned to past noise) and unmodeled execution reality (slippage, latency, downtime, rejected orders). Closing that gap is the real work.

For anything time-sensitive or that has to run 24/7, yes — a sleeping laptop or a home-internet outage means missed fills. For a slow strategy you trigger manually, a reliable desktop is fine. Either way, measure your real latency before paying for a location.

We operate TradoxVPS and provide trading infrastructure, not financial advice. Algorithmic trading carries substantial risk, including the total loss of capital, and backtested performance never guarantees live results.