Search “best high-frequency trading algorithms” and you’ll get two flavors of answer, both useless. One is breathless hype that makes HFT sound like a secret money printer guarded by quants in a vault. The other is a sales page implying you can run it from a budget VPS if you just buy their plan. Neither is true, and the real picture is more interesting than either.

Here’s the thing almost nobody leads with: the algorithms themselves are mostly well understood and, frankly, not that exotic. The firms that win at high-frequency trading are not winning on secret mathematics. They’re running a handful of well-known strategies and winning on speed, executing the same ideas microseconds faster than everyone else. That single fact reframes the whole topic, and it’s where we’ll start.

This is an honest tour of the actual HFT algorithm families. What each one does, how it makes money, the infrastructure it genuinely requires, where the legal line sits, because several “strategies” you’ll read about online are outright crimes, and the part most articles skip entirely: what a serious independent or proprietary trader can and can’t realistically run without an institutional budget.

The uncomfortable truth: it’s a speed race, not a secret-algorithm race

Before the list, the framing that makes the list make sense.

Most practical high-frequency trading strategies are, at their core, fairly simple arbitrages, the kind that could have been performed at lower frequency in an earlier era. What changed isn’t the cleverness of the math. It’s that the competition moved to who can execute a known idea the fastest, rather than who can invent a new one. When fifty firms all understand the same arbitrage, the one who acts first takes the profit and the rest get nothing, so the entire contest collapses into a race measured in microseconds and increasingly nanoseconds.

That’s why the genuine moat in HFT is infrastructure, not insight. The serious players spend on field-programmable gate arrays that execute trading logic in hardware rather than software, on colocation cabinets inside the exchange’s own data center, on kernel-bypass networking that skips the operating system’s overhead, and on direct market access that removes intermediaries from the order path. The strategy is the easy part. The speed is the expensive part, and the speed is institutional. Keep that in mind as we go through the families, because for each one the question that actually decides whether you can run it isn’t “do I understand it” but “can I be fast enough.”

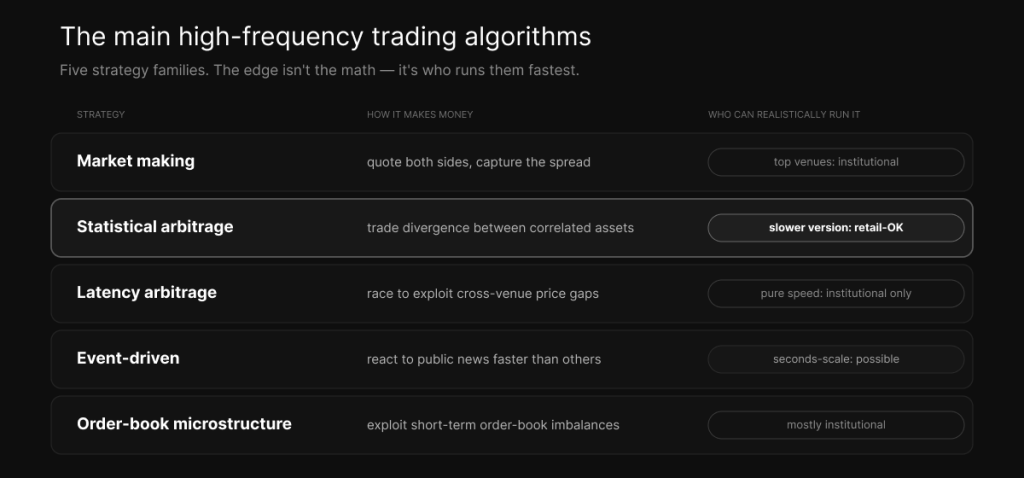

Market making: the dominant strategy

If HFT has a flagship strategy, it’s market making, also called liquidity provision, and it’s the most common thing high-frequency firms actually do.

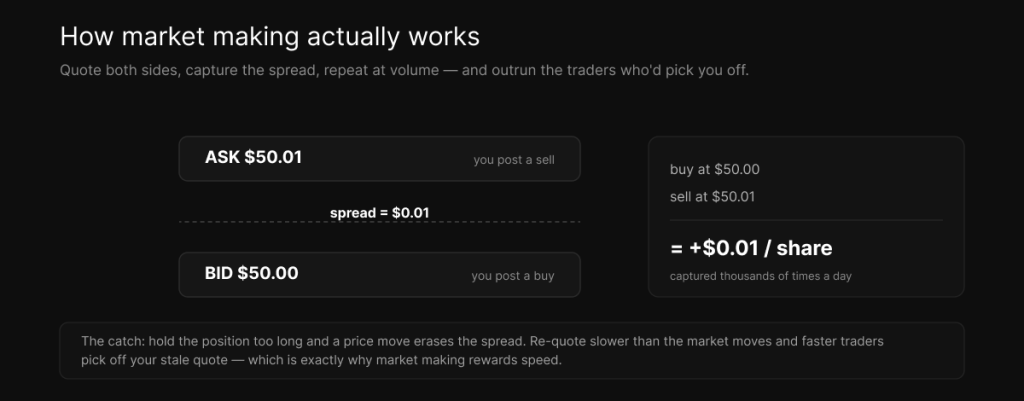

The mechanism is simple to describe. The algorithm continuously posts both a buy order slightly below the current price and a sell order slightly above it, and profits from the gap between them, the bid-ask spread. Buy at 50.00, sell at 50.01, and you’ve made a cent a share. A cent sounds like nothing, and on a single trade it is, but repeated across enormous volume it adds up, and many venues sweeten the deal with rebates or reduced fees for providing liquidity, which stack on top of the spread. Worth noting: HFT market makers usually carry no formal obligation to keep quoting, unlike registered market makers, so they can pull their quotes the instant conditions turn against them.

The danger in market making is inventory risk. Every time you buy without an offsetting sale, you’re holding a position, and if the price moves against that position before you can offload it, the loss can swallow many cents of spread at once. Managing that inventory in real time, deciding when to widen quotes, pull them, or hedge, is most of the actual difficulty.

This is also where speed becomes survival rather than just advantage. Your resting quotes are a standing offer to the rest of the market, and a faster trader who sees the price about to move can hit your stale quote before you’ve had a chance to cancel it, a problem called adverse selection, or getting picked off. To avoid that you need to update and cancel your quotes faster than the market moves and faster than the predators watching you. On the most liquid, most contested instruments, the E-mini S&P 500, major stocks, that speed requirement is brutal, which is why those venues are dominated by colocated firms and why a retail trader has essentially no chance of competing there. On slower or less-contested venues the math softens a little, but make no mistake, market making is fundamentally a speed game.

Statistical arbitrage and mean reversion

This family is the most quantitative of the bunch and, importantly, the most accessible to traders without a microsecond budget.

The idea rests on stable statistical relationships between instruments. Two correlated stocks, a futures contract and the basket of things it tracks, related currencies, instruments that historically move together tend to keep moving together. Statistical arbitrage watches the relationship and acts when it temporarily breaks: when the spread between two normally-correlated assets stretches wider than usual, the algorithm bets it will snap back, going long the one that’s lagged and short the one that’s run ahead, then closing both legs when the relationship reverts to its normal range. It’s mean reversion applied to relationships rather than single prices, executed systematically across many pairs at once to smooth out the cases where the relationship simply breaks for good.

The crucial point for anyone reading this without a colocation budget is that statistical arbitrage spans a huge range of timescales. At the fast end it’s an HFT strategy fighting over millisecond divergences, and there you’re back in the institutional speed race. But at slower timescales, divergences that play out over minutes, hours, or days, it doesn’t require winning a microsecond contest at all. It requires good models, clean data, and reliable execution. This slower end of statistical arbitrage is genuinely where a serious independent or proprietary trader can compete, because the edge comes from the quality of the model and the discipline of the execution rather than from being the single fastest participant on the wire. A low-latency setup still helps you get filled at better prices, but it isn’t the whole game the way it is for the pure-speed strategies.

Latency arbitrage: the purest speed play

Latency arbitrage is HFT distilled to its essence, and it’s the strategy you should most firmly forget about running yourself.

The same asset, or two tightly linked assets, often trades in more than one place: a stock on multiple exchanges, a futures contract and its underlying index, the same instrument across venues in different cities. For brief moments after a price moves in one place, the other places haven’t caught up yet, and a price gap opens. Latency arbitrage races to exploit that gap, buying where the price is still low and selling where it’s already high, before the venues re-synchronize and the gap closes. The window is measured in microseconds, so the only thing that matters is being faster than every other firm trying to do the exact same thing.

The canonical example is the corridor between Chicago and New York, where CME futures and New York equity markets are linked, and where firms have spent hundreds of millions of dollars on dead-straight fiber and line-of-sight microwave networks to shave milliseconds, then microseconds, off the trip between the two. That arms race is the clearest illustration in all of finance that latency arbitrage is a pure infrastructure contest, and it’s an unwinnable one for anyone without that infrastructure. On a retail connection you would not be the arbitrageur; you’d be the slow participant whose stale prices are being arbitraged. We get into why distance, not bandwidth, decides this in network speed vs latency and why a Chicago VPS is best for CME futures.

Event-driven and news trading

This family trades the reaction to information rather than the structure of the order book.

Scheduled economic releases, the jobs report, inflation data, central bank decisions, move prices sharply and predictably in their timing, if not their direction. Event-driven strategies position to trade the immediate move the instant the data hits. At the extreme institutional end, firms ingest machine-readable news feeds and react in microseconds, parsing the number and firing orders before a human could finish reading the headline. That microsecond version is, again, an institutional capability.

But there’s a slower version of event-driven trading that is reachable. Reacting to a release in seconds rather than microseconds, with a systematic rule about how to position around scheduled volatility, doesn’t require beating the news-parsing machines, it requires being faster and more disciplined than the broad mass of slower participants. A low-latency, stable connection helps here by making sure you’re not at the very back of the queue when the market lurches, even if you’re never going to be at the very front.

Order-book and microstructure strategies

The last legitimate family lives entirely inside the mechanics of the order book.

These strategies exploit very short-term structure: temporary imbalances between resting buy and sell orders, the dynamics of queue position, patterns that hint at hidden size like iceberg orders that reveal only a fraction of their true quantity. A close cousin is order anticipation, detecting that a large order is working its way through the market and positioning ahead of the price impact it will cause. There’s an important legal nuance here that’s easy to get wrong: anticipating a publicly visible market signal is legal, but front-running a specific client’s order when you owe that client a duty is illegal. The legitimate version reads public information faster and reacts; it doesn’t abuse a privileged position. Like the other speed-dependent families, this is mostly an institutional game, because the edges are tiny and vanish in microseconds.

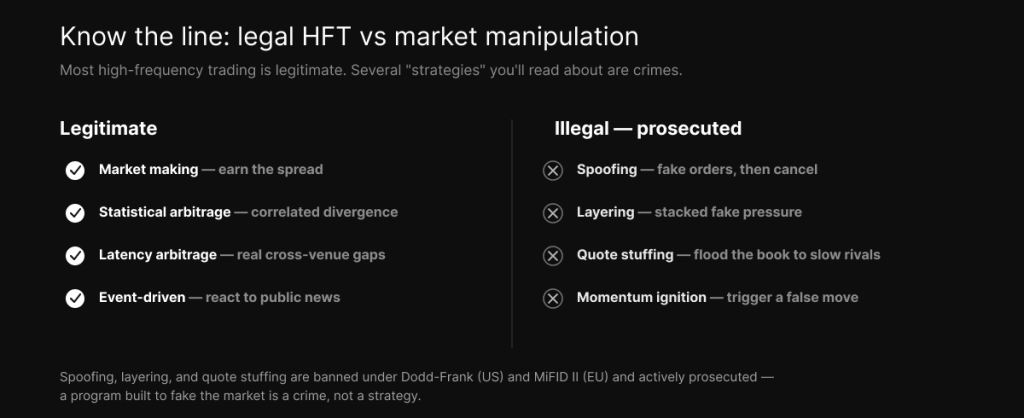

The strategies that are actually illegal

Here’s the section the hype articles leave out, and the one that matters most for staying out of prison. Several techniques described online as clever “HFT strategies” are market manipulation, expressly illegal, and actively prosecuted. They are not advanced methods to study and adopt. They are crimes.

Spoofing is placing large orders you have no intention of executing, in order to create a false impression of supply or demand and trick other participants into trading the way you want, then canceling before your fake orders fill. Under the Dodd-Frank Act, spoofing is defined as bidding or offering with the intent to cancel before execution, and doing it knowingly is a felony. The most famous case is Navinder Sarao, charged in connection with the 2010 Flash Crash, who ran spoofing software from a house in suburban London.

Layering is a form of spoofing that stacks multiple fake orders at different price levels to simulate building pressure in one direction, luring others to follow before the whole stack is canceled. It’s been prosecuted and fined repeatedly. Quote stuffing floods the market with thousands of orders and cancellations per second, not to fake a price but to overload the exchange’s systems and slow competitors down, exploiting the congestion to gain a latency edge. Regulators treat it as manipulation. Momentum ignition deliberately triggers a sharp price move to set off other traders’ momentum systems, then profits as the move plays out or rebounds, and regulators have flagged it as a manipulative practice too.

All of these are banned under Dodd-Frank in the United States and MiFID II in the European Union, and enforcement has gotten more aggressive, not less. The regulator’s own framing draws the line cleanly: lawful algorithmic trading is completely fine, but a computer program written to fake the market is illegal and will be prosecuted. If a “strategy” depends on placing orders you intend to cancel or on deceiving other participants about real supply and demand, it’s not a strategy you want anywhere near your account.

What you can actually run

So where does that leave a serious trader who isn’t a hedge fund? With a clear and honest picture, which is more than most pages will give you.

True microsecond high-frequency trading, the latency arbitrage, the top-tier market making on the most contested instruments, the microsecond news parsing, is an institutional arms race. It runs on colocation cabinets inside the exchange data center, on FPGAs and kernel-bypass networking and the fastest fiber and microwave links money can buy, and it costs a five- or six-figure monthly budget to even participate. You cannot do that from a retail VPS, full stop, and any hosting provider implying otherwise is selling you a fantasy. We’ve been blunt about this throughout, because the honest version is the one that actually protects you: a retail VPS is not colocation, and microseconds belong to a tier you’re not buying into.

What you can run is the latency-sensitive, slower-timescale end of these same ideas. Slower statistical arbitrage where the edge is your model, not your wire speed. Systematic strategies that benefit from low latency and rock-solid stability but don’t need to win a microsecond race to be profitable. Faster-timeframe automated trading where being physically close to the exchange genuinely improves your fills and your queue position without pretending you’re colocated. The realistic and achievable goal is to be as fast and as stable as retail trading practically gets, not to go toe-to-toe with the firms that spent a fortune to be the fastest object on the network. For futures specifically, that means a Chicago-metro VPS near CME gets you a short, honest path to the matching engine, which is a real edge for the strategies you can actually run, and irrelevant to the ones you can’t.

So what infrastructure do you actually need?

For the accessible strategies, the shopping list is short and it doesn’t include FPGAs or a colocation contract. You want a low-latency VPS physically close to your venue, the Chicago metro for CME futures, so your network leg to the exchange is as short as retail allows. You want a fast single-thread CPU for the decide-and-send loop, because the strategies you can run lean on clock speed more than core count. You want low jitter and near-zero packet loss so your timing stays consistent, which matters more for a systematic strategy than a flashy headline latency number, as we cover in network speed vs latency. And you want reliable, monitored uptime so an automated strategy isn’t left stranded mid-session.

That’s the right tier for the trader you actually are. Measure your own latency rather than trusting anyone’s marketing, match your infrastructure to the strategies you can realistically run, and don’t pay for microseconds you have no way to use. Plans and pricing are here once you know what you’re actually building.

Frequently asked questions

Market making, also called liquidity provision. The algorithm continuously quotes both a bid and an ask and profits from the spread between them, repeated across enormous volume, often with exchange rebates on top. It’s the workhorse strategy of most HFT firms.

Mostly no. The strategies are well understood and many are fairly simple arbitrages. The genuine competitive edge in high-frequency trading is execution speed, not secret mathematics, which is why firms compete on infrastructure like colocation and FPGAs rather than on inventing new strategies.

Not true microsecond HFT, which requires colocation inside the exchange data center, specialized hardware, and direct market access, all of which are institutional. What you can run on a fast, low-latency VPS is latency-sensitive systematic trading on slightly slower timescales, where a close, stable connection improves your fills without needing to win a microsecond race.

Most of it is. Market making, arbitrage, statistical arbitrage, and event-driven trading are legitimate strategies that exploit real market inefficiencies. However, spoofing, layering, quote stuffing, and momentum ignition are market manipulation, illegal under Dodd-Frank and MiFID II, and actively prosecuted. The line is whether the strategy deceives other participants or places orders you intend to cancel.

High-frequency trading is a subset of algorithmic trading defined by ultra-fast execution, very short holding periods, and high turnover. Algorithmic trading is any rule-based, computer-driven trading, including strategies that hold positions for hours, days, or longer and have no speed requirement at all.

For true HFT, microseconds, which is an institutional capability. For the latency-sensitive systematic strategies a serious retail or proprietary trader can realistically run, low single-digit milliseconds from a VPS close to your exchange is a strong, honest target. Measure your real order round trip rather than trusting an advertised ping.

For genuine microsecond HFT, yes, firms execute logic in hardware to shave nanoseconds. For the strategies accessible to retail and proprietary traders, no. A fast, stable CPU-based VPS close to your venue is the appropriate and sufficient tier.

We operate TradoxVPS and provide trading infrastructure, not financial or legal advice. This article is educational and is not an endorsement of any strategy; manipulative practices such as spoofing and layering are illegal. Trading futures and other leveraged products carries substantial risk, including the loss of more than your initial deposit.